The Central Banks of Switzerland, Canada and the EU have rocked the markets…but the most important question in Central Bank land is, ”Will the Fed still raise interest rates in 2015?” Our view has been that global Central Banks…despite all their “money printing”… are losing the fight against deflation…that “Currency Wars” are just passing the “hot potato” of deflation from one country to another. In his famous (helicopter money) speech in November 2002 Ben Bernanke defined deflation as a “Collapse in demand.” Well crude oil, copper and the major commodity indices, as well as CAD and the AUD are at 6 year lows…and as Dennis Gartman likes to say, “When a market is going down you have no idea how far down, down is!”

Whether or not the Fed will raise interest rates is the KEY question because the assumed “Divergence” between America and the Rest of the World has helped drive the US Dollar Index to 12 year highs. If the market begins to think that the Fed will not raise rates…for all the obvious reasons…then we’d expect to see a USD correction.

US Dollar Index:

Canadian Dollar: is down ~25% since the commodity boom peaked out in 2011…it’s down ~15% since July 2014…when Crude began its waterfall decline. Last week…before the Bank of Canada cut interest rates…the market was pricing in a 20% chance of an interest rate cut in 2015…it’s now pricing in a 50% chance of ANOTHER interest rate cut in 2015. Pressure on CAD rises exponentially the more Crude Oil falls….BUT…

The Bank of Canada action helped drive the Toronto Stock Index 500 points higher…and drive the Canadian 10 year bond to All Time Highs…

The ECB action has helped drive the German DAX and the German 10 year bond to All Time Highs…

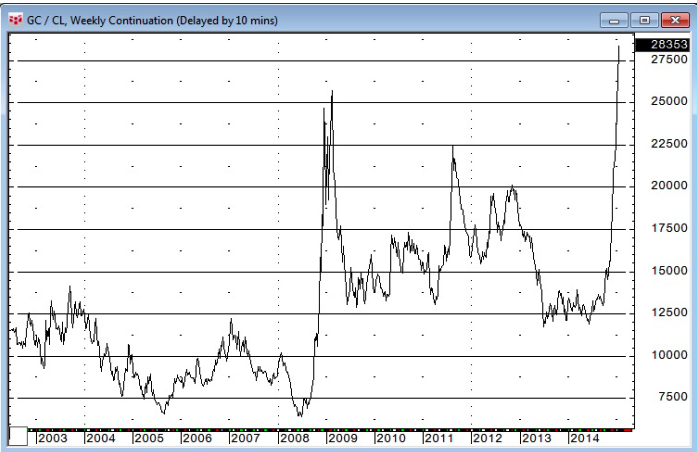

Gold: is up ~$170 (15%) from 4 year lows made last November…gold share indices are up ~30%…as higher gold and lower oil dramatically improve the leverage for gold miners. Last July it took only 12 barrels of WTI to buy 1 ounce of gold…it now takes 28 barrels. Another “consequence” of global deflation and a surging US Dollar may be that “Resource Nationalism” will, by necessity, become a thing of the past…thereby making it easier and cheaper for gold mining companies to operate in many formerly “difficult” countries.

Short term trading: The best results in our Model account YTD have come from short call positions in CAD and AUD. Our worst results came from short OTM puts on the CAD after it had fallen more than 3 cents in 2 weeks…after option vol had surged to 3 year highs and as crude oil looked like it was “stabilizing” around $47…BUT…we hadn’t expected the Bank of Canada to drive CAD to 6 year lows. It “feels” like we should have made good profits this month given the market action…but we are grateful we didn’t get clobbered by some of those same moves!

Long term trading: I’ve made more money over the last 3 – 4 years from my long term hedges against the CAD than from all of my short term trading. I’m especially grateful that I was able to buy more USD last fall…it was hard to do because CAD had dropped below 90 cents and I was selling new lows…but I was able to take the perspective that the ten year “Commodity boom” was over…and the “Big Risk” was that CAD might take out the 2009 lows.