With the failure to even vote on the “repeal and replace Obamacare,” coupled with the ongoing investigations into the White House “Russian” connections we thought it apropos to revisit the Presidential cycle. The Presidential cycle has historically had an impact on the stock markets and the economy. According to the Stock Trader’s Almanac (Jeffery A. Hirsch & Yale Hirsch) that is published annually, wars, recessions, and bear markets tend to occur in the first half of the four-year term while more prosperous times and bull markets tend to appear in the latter half. According to the Hirschs of the 45 administrations since 1833, the second-half stock market gains have been 729.1% vs. a gain of only 307.1% in the first half.

One might even argue that the most recent President, despite all the maligning, did quite well beating the odds in the usually weak post-election year and mid-term year but underperforming during the latter two years the pre-election year and the election year. His first two years saw the Dow Jones Industrials (DJI) gain 36.5% (2009-2010) and 36.0% (2013-2014). His latter two years produced gains of 13.1% (2011-2012) and 11.2% (2015-2016) respectively.

Given some signs of trouble early on in his Presidency, will President Trump do as well? His Republican predecessor George W. Bush is one of the few Presidents who actually saw the stock market lower when his term was over in 2008. From 2001 to 2008, the DJI lost 18.6%.

The cycle is not always perfect. The well-known four-year stock market cycle often sees its low occur during the Presidential cycle although they do not necessarily line up. Given we suspect the last four-year cycle low was seen in August 2015 the next one won’t be due (in theory) until 2018–2020 in the latter half of President Trump’s term of office. The question always is, “when does the top come in.” Tops can skew left, center, or right. In March 2017, the market is already 18 months up in the current bull cycle.

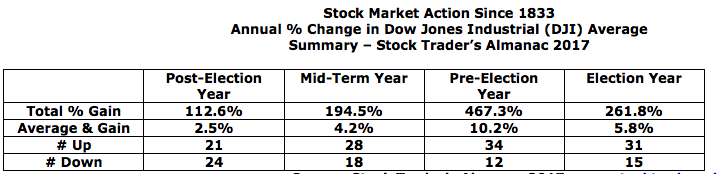

The following summarizes the stock market action since 1833.

Source: Stock Trader’s Almanac 2017 www.stocktradersalmanac.com

It is rare to see the stock market up four years in a row during one President’s term. It has occurred four times since 1833. They were Calvin Coolidge (Republican) 1925–1928, Franklin Roosevelt (Democrat) 1933–1936, Ronald Reagan (Republican) 1985–1988 and Bill Clinton (Democrat) 1993–1996. Only one President saw four consecutive losing years and that was Herbert Hoover (Republican) 1929–1932.

As to the biggest winner and biggest loser Woodrow Wilson (Democrat), 1913–1920 saw an 81.7% increase in the DJI in 1915, while Herbert Hoover (Republican) 1929–1932 saw the market collapse 52.7% in 1931. Since 1949, the President that saw the biggest gain during his term was Bill Clinton (Democrat) 1993–1996 with an incredible 109.9% gain in his first four-year term. The biggest loser was George W. Bush (Republican) 2005–2008 with a 21.4% loss during his second four-year term.

We went a few steps further with our study from 1949 and besides the stock market we also looked at GDP growth, debt growth, the debt to GDP ratio, gold, the US$ Dollar Index, and recessions.

The GDP growth winner was Jimmy Carter (Democrat) 1977–1980 with a GDP growth gain of 52.5% during his term. The weakest GDP growth occurred under Barrack Obama (Democrat) 2009–2012 with a gain of 9.8% following the steepest recession on record (2007–2009) since the Great Depression. As to debt, the Great Communicator Ronald Reagan (Republican) 1981–1984 and 1985–1988 saw the largest percentage debt growth with gains of 73.2% and 65.5% respectively. While Barrack Obama (Democrat) 2009–2012 and 2013–2016 saw the national debt grow from $10.7 trillion at the end of 2008 to $19.9 trillion by the end of 2016 it was only a gain of 86%, less than Ronald Reagan’s gain of 189% during his two terms. As to the Presidents that contained debt growth the best, it is noteworthy that Presidents Truman (Democrat), Eisenhower (Republican), and Kennedy (Democrat) saw only low growth in the debt under 10%. Since then, only one President has accomplished that and that was Bill Clinton (Democrat) 1997–2000 that saw the national debt only grow by 8.6%.

The debt-to-GDP ratio fell steadily from Truman (Democrat) through Carter (Democrat) and did not start rising again until Ronald Reagan (Republican). Since then the debt-to-GDP ratio has climbed steadily with only Bill Clinton’s (Democrat) second term seeing a decline. Today, the US debt-to-GDP ratio is over 100 and that alone becomes a permanent drag on the economy.

Market Action Since 1949 Presidential Cycle

|

Elected President |

Stock Market % Gain (Loss) DJI |

GDP % Gain (Decline) |

Debt % Gain (Decline) |

Debt to GDP (End of Term %) |

Gold % Gain (Loss) |

US$ Index % Gain (Loss) |

Four-Year Cycle Low |

Recessions Duration GDP % Decline |

Stock Market Bears (Loss %) Minimum 10% – DJI |

US at War |

|

Truman (D) 1949-1952 |

50.3 |

33.8 |

2.7 |

70.4 |

9.6 |

1949 |

Nov 1948-Oct 1949 11 Mths (1.7%) |

June 1948-June 1949 (16.3%) |

Korean War 1950-1953 |

|

|

Eisenhower (R) 1953-1956 |

75.5 |

22.3 |

5.3 |

60.6 |

0.8 |

1953 |

July 1953-May 1954 10 Mths (2.6%) |

Jan 1953-Sep 1953 (13.0%) |

Suez Crisis 1956 Vietnam 1955-1964 |

|

|

Eisenhower (R) 1957-1960 |

32.4 |

20.7 |

5.0 |

52.7 |

0.8 |

1957 |

Aug 1957-Apr 1958 8 Mths (3.7%) |

Apr 1956-Oct 1957 (19.4%) Jan 1960-Oct 1960 (17.4%) |

Vietnam 1955-1964 Lebanon Crisis 1958 |

|

|

Kennedy/Johnson (D) 1961-1964 |

41.8 |

26.3 |

8.9 |

45.4 |

(0.5) |

1962 |

Apr 1960-Feb 1961 10 Mths (1.6%) |

Dec 1961-Jun 1962 (27.1%) |

Bay of Pigs Cuba 1961 Cuban Missile Crisis 1962 Laos 1962-1975 |

|

|

Elected President |

Stock Market % Gain (Loss) DJI |

GDP % Gain (Decline) |

Debt % Gain (Decline) |

Debt to GDP (End of Term %) |

Gold % Gain (Loss) |

US$ Index % Gain (Loss) |

Four-Year Cycle Low |

Recessions Duration GDP % Decline |

Stock Market Bears (Loss %) Minimum 10% – DJI |

US at War |

|

Johnson (D) 1965-1968 |

4.4 |

37.5 |

11.5 |

36.9 |

10.2 |

1966 |

Feb 1966-Oct 1966 (25.2%) |

Dominican Republic 1965 USS Liberty 1966 Laos, Cambodia 1968 |

||

|

Nixon (R) 1969-1972 |

9.7 |

36.0 |

22.9 |

33.3 |

65.2 |

1970 |

Dec 1969-Nov 1970 11 Mths (0.6%) |

Dec 1968-May 1970 (35.9%) Apr 1971-Nov 1971 (16.1%) |

Cambodia 1970 Vietnam 1966-1975 |

|

|

Nixon/Ford (R) 1973-1976 |

(5.6) |

46.5 |

45.2 |

33.0 |

111.7 |

(13.0) |

1974 |

Nov 1973-Mar 1975 1 Yr 4 Mths (3.2%) |

Jan 1973-Dec 1974 (45.1%) |

Laos, Vietnam, Cambodia to 1975 |

|

Carter (D) 1977-1980 |

0.2 |

52.5 |

46.3 |

31.7 |

337.0 |

(3.2) |

1978 |

Jan 1980-July 1980 6 Mths (2.2%) |

Sep 1976-Feb 1978 (26.9%) Sep 1978-Apr 1980 (16.4%) |

Iran Hostage Crisis 1980 |

|

Reagan (R) 1981-1984 |

26.4 |

41.2 |

73.2 |

38.9 |

(47.8) |

35.2 |

1982 |

Jul 1981-Nov 1982 1 Yr 4 Mths (2.7%) |

Apr 1981-Aug 1982 (24.1%) |

Libya 1981 Sinai 1982 Lebanon 1982 Grenada 1983 |

|

Reagan (R) 1985-1988 |

82.4 |

30.0 |

65.5 |

49.5 |

33.2 |

(26.8) |

1987 |

Nov 1983-Jul 1984 (15.6%) Aug 1987-Oct 1987 (36.1%) |

Libya 1986 Honduras, Nicaragua, Iran Contra 1983-1989 Persian Gulf 1987-1988 |

|

|

Bush 1 (R) 1989-1992 |

45.4 |

24.5 |

56.2 |

62.2 |

(18.8) |

Flat |

1990 |

Jul 1990-Mar 1991 8 Mths (1.4%) |

Jul 1990-Oct 1990 (21.2%) |

Libya 1989 Panama 1989, Gulf War 1 1990 Iraq 1991 |

|

Clinton (D) 1993-1996 |

109.9 |

23.9 |

28.5 |

64.5 |

10.8 |

(1.1) |

1994 |

Bosnia Herzegovina 1992-1996 Iraq 1992-2003 Somalia 1992-1995 Bosnia 1993-1995 |

||

|

Clinton (D) 1997-2000 |

55.0 |

27.0 |

8.6 |

55.2 |

(26.3) |

20.2 |

1998 |

Jul 1998-Aug 1998 (19.3%) |

Iraq 1998 Afghanistan Sudan 1998 Serbia Kosovo 1999 Yemen 2000 |

|

|

Bush 2 (R) 2001-2004 |

(0.5) |

19.4 |

30.1 |

60.1 |

61.0 |

(6.9) |

2002 |

Mar 2001-Nov 2001 8 Mths (0.3%) |

Jan 2000-Sep 2001 (29.7%) Mar 2002-Oct 2002 (31.5%) |

9/11 2001 Afghanistan 2001 to present Gulf War 2 2003-2011 Haiti 2004 |

|

Bush 2 (R) 2005-2008 |

(21.4) |

19.9 |

35.9 |

68.1 |

102.1 |

(2.1) |

2008 |

Dec 2007-Jun 2009 1 Yr 6 Mths (4.3%) |

Oct 2007-Mar 2009 (53.8%) |

Lebanon 2006 Somalia 2007 |

|

Obama (D) 2009-2012 |

64.8 |

9.8 |

60.3 |

99.5 |

89.6 |

(12.6) |

2011 |

Apr 2011-Oct 2011 (16.8%) |

Yemen 2010 – 2017 Iraq 2011-2017 |

|

|

Obama (D) 2013-2016 |

50.8 |

15.7 |

21.6 |

104.8 |

(31.2) |

24.1 |

2015 |

May 2015-Aug 2015 (16.2%) Nov 2015-Jan 2016 (14.1%) |

Syria 2012-2017 Iraq 2011-2017 Uganda Somalia 2014-2017 ISIS 2014-2017 Persian Gulf 2015, South China Sea 2015-2017 Balkans Ukraine 2014-2017 |

|

|

Trump (R) 2017-2020 Note1 |

4.9 |

0.4 |

0.5 |

104.8 |

8.4 |

(2.0) |

Iraq, Syria, ISIS, Persian Gulf, North Korea, South China Sea, Yemen, Balkans, Ukraine |

|||

|

Total Gain % |

10,160 |

6,426 |

7,595 |

4,065 |

(8.3) |

Source: David Chapman

Note1: To March 30, 2017 only

Official recessions have occurred under almost every President since 1950. Some, however, managed to avoid any official recession. No official recession occurred under Johnson (Democrat) 1965–1968, Reagan (Republican) 1985–1988, Clinton (Democrat) in both 1993–1996 and 1997–2000, and under Obama (Democrat) also twice 2009–2012 and 2013–2016. The steepest recession occurred under George W. Bush (Republican) 2005–2008 with the official recession from October 2007 to June 2009 (overlapping into Obama’s first term) when the economy contracted 4.3%. That was also the longest official recession.

Gold was largely held at $35/ounce until Richard Nixon (Republican) ended the Bretton Woods agreement in August 1971, taking the world off the gold standard and setting gold to trade freely. Currencies were set to trade freely or float against the world’s reserve currency the US$ in 1973 following the Smithsonian Agreement. The history of the US$ Index begins then.

It probably comes as no surprise that gold’s biggest gains came during the term of Jimmy Carter (Democrat) 1977–1980. Gold gained 337% during that term. Nobody has been close since, although during George W. Bush’s (Republican) second term 2005–2008 gold gained 102.1%. The US$ Index tends to fall when gold rises and vice versa. The US$ Index has lost 8.3% of its value since it began in 1973. Its biggest decline during a Presidential term was under Ronald Reagan’s (Republican) second term 1985–1988 when it fell 26.8%. Ronald Reagan (Republican) 1981–1984 also saw the biggest gain for the US$ Index as it jumped 35.2% during his first term.

So what can we conclude out of all of this? And how will it potentially impact President Trump’s term? Given that there has been no official recession since the Great Recession of 2007–2009, the odds would seem to favour a recession occurring in the next four years. There is no record of three successive Presidential terms with no recessions. Stock markets tend to perform better under Democrat presidents (average 47.2% gain/term for Democrats vs. average 27.1% gain/term for Republicans). With stellar gains in the past two Presidential terms, could bumps be coming to the stock market?

GDP growth is a bit of a wash with no one party seeming to have an advantage. Under Democratic Presidents since 1949, GDP growth has averaged 28.3% per term while under Republican Presidents it has averaged 28.9% per Presidential term. With debt, however, the Republicans are the biggest debt creators. Under Democratic Presidents, debt growth has averaged 23.6% per Presidential term while under Republican Presidents the debt has grown 37.7% per Presidential term. Gold has seen its strongest gains under Democratic Presidents with an average gain per term of 49.9% vs. 34.2% gains under Republican Presidents. The US$, however, tends to fall under Republican Presidents losing 1.6% on average during their terms vs. a gain of 5.5% under Democrat Presidents per term.

We included a column of US involvement in war. Of its 241 years of existence, the US has been at war or involved in a war in 224 of those years or 93% of the time. Since 1949, the US has been involved in or at war almost continually.

If we were to make a prediction based on the history of the Presidential cycle for President Trump, we would say that the stock markets should underperform while GDP growth should bump along. However, odds favour a recession during the next four years, debt should grow considerably, the US$ Index should fall, and gold should rise. And, the US will be at war somewhere with someone.

Source: www.goldchartsrus.com

Charts and commentary by David Chapman

Phone: 416-523-5454 Email: david@davidchapman.com

Copyright David Chapman 2017

Disclaimer

David Chapman is not a registered financial advisor, nor an exempt market dealer (EMD). We do not and cannot give individualized market advice. The information in the newsletter is only intended for informational and educational purposes. It should not be considered a solicitation of an offer or sale of any security. The reader assumes all risk when trading in securities and David Chapman advises consulting a licensed professional financial advisor before proceeding with any trade or idea presented in this newsletter. David Chapman may take a position and sell a position in any security mentioned in this newsletter. We share our ideas and opinions for informational and educational purposes only and expect the reader to perform due diligence before considering taking a position in any security. That includes consulting with your own licensed professional financial advisor.