Recently the Stock Market moves down are fast and deep. This shows a way to make money from falling stock prices, and the process of identifying stock market dogs to protect yourself from a rising market – Ed.

I get a lot of questions about short selling, probably because most investors have never done it.

Short selling is the sale of a stock that is not owned by the seller in anticipation that the stock’s price will decline, enabling it to be bought back at a lower price to make a profit. If you can identify stocks before they fall, you can make a bundle of money via short selling.

To help you understand the mechanics and opportunity of short selling, I want to walk you through my most recent successful short sale to help you decide if short selling is right for you.

On April 7 of this year, I sent out this alert to my Rational Bear subscribers, telling them to “short” Conn’s, Inc. (CONN).

Conn’s is a large furniture and appliance retailer, but what’s unusual about it is the fact that it both sells furniture/appliances and loans its customers the money to buy its furniture/appliances. Sort of like General Motors and General Motors Acceptance Corporation (GMAC).

On the surface, Conn’s appeared to be growing quite well by selling an increasing number of products, but it was doing so by extending credit to just about any deadbeat that walked through its doors.

You and I may not need to borrow money to buy a washing machine or a color TV… but 80% of Conn’s customers do. Those are the kind of people I grew up with, and while they may be decent people, they are not the kind of people I’d want to loan money to.

That strategy started to backfire when the Conn’s finance division reported a massive $43.2 million quarterly loss. At the time, I said, “Those credit losses are going to get worse.”

How did I know that?

- The number of loans that were more than 60 days past due jumped to 9.9%.

- Most businesses reconsider their lending practices when bad loans skyrocket, but not Conn’s. Instead, it was loaning more than ever; accounts receivable increased by 16% to $743.9 million at the end of the first quarter.

- Conn’s increased its provision for bad debts by 11% to $64.8 million, but that wasn’t enough, considering the pace its customers were defaulting.

Those were serious red flags, but the biggest warning sign was the “creative accounting” Conn’s used to make its business appear better than it really was.

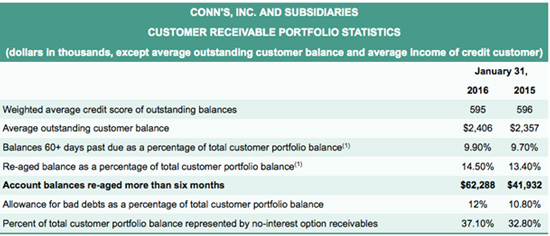

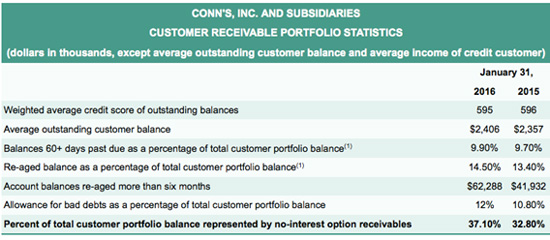

Accounting Trick #1: Re-Aging Bad Debt. There is a little-used but legal accounting practice called “re-aging” debt. It is used to reclassify deadbeat loans into not-deadbeat loans. Basically, when an account is re-aged, it is no longer considered to be past due.

In the first quarter of 2016, Conn’s “re-aged” $21 million worth of loans—from $41.93 million to $62.29 million.

Accounting Trick #2: No-Interest Option Receivables. A typical loan payment is part principal and part interest, just like a home mortgage. However, when a struggling customer can’t afford to make the full payment, a loan company may let the customer get by just paying the interest on the loan.

But when a customer is really in trouble, a loan company could temporarily waive both principal and interest payments. In short… pay nothing!

Why would a loan company do this? Because it keeps the loan from being reclassified as a bad debt, which makes the loan portfolio look better than it really is.

In the first quarter of 2016, the percentage of Conn’s loans converted to no-interest loans rose from 32.8% to 37.1%.

Okay, here is what really counts: Nearly 80% of Conn’s sales are financed through its own in-house credit business.

My expectation was for one of two things to happen… and both of them were very bad:

Bad (but Fast) Outcome #1: Conn’s would tighten up its credit practices and extend much less credit. In that case, the 80% of its customers that couldn’t pay cash simply wouldn’t buy. Revenues would collapse, and Conn’s would report massive losses.

Bad (but Slow) Outcome #2: Conn’s would continue to make loans to anybody that could fog a mirror, and its credit losses from bad loans would skyrocket. Revenues would continue to show modest growth, but Conn’s would report massive losses from massive defaults.

Conn’s sort of let the cat out of the bag when it told Wall Street to tone down its full-year expectations. The company now expects revenues to grow by mid- to high single digits, well below Wall Street’s insane expectations for 13% sales growth, but I thought even that was too high.

Conn’s closed at $10.48 the day I sent out my trading alert, but its stock dropped like a rock on June 2, 2016, when it reported a much-bigger-than-expected loss of $0.31 per share—which shocked the Wall Street crowd that was expecting only a $0.06 profit!

The problem (no surprise) was that the number of deadbeat loans had increased and generated a $21 million operating loss, which pushed the bad-debt ratio from 14.25% to 15.25%.

That’s a huge number of deadbeat loans, which is why CEO Norm Miller said that Conn’s would have to make a commitment to “increased investment in credit risk management.”

Conn’s expects the rest of the year to get even worse. It lowered its mid-to-single-digit revenue growth forecast to low to mid-single digits.

And just for good measure, Conn’s fired its CFO and brought in a fresh face to tackle its financial woes.

Conn’s shares plummeted on that news, and we closed out the Conn’s short sale with a 21% profit, which is pretty darn good considering that the stock market had done nothing but pretty much go straight up during this time (April 7 to June 2).

That’s a fat gain, but short selling can be even more lucrative when the next bear market comes around.

My goal of showing you the anatomy of the Conn’s short sale is not to pat myself on the back, but to show you the process of identifying stock market dogs and a way to make money from falling stock prices.

Short selling isn’t a complicated, esoteric practice reserved for hedge funds and institutional investors. It’s not only a valuable diversification tool that helps you make money, but a defensive bear market insurance policy. Give Rational Bear a risk-free 3-month try and see for yourself.

Tony Sagami

related: Short Selling: A Trader’s Guide