It’s a huge morning for the US economy.

At 8:30 a.m. ET, the Bureau of Economic Analysis will release its first reading on first-quarter gross domestic product, which is expected to show the economy grew at just a 1% pace in the first quarter.

This announcement will be followed at 2 p.m. ET by the Federal Reserve’s latest monetary policy announcement.

In March at its most recent meeting, the Fed said it would not look to raise interest rates at the April meeting.

Moreover, Federal Reserve Chair Janet Yellen will not speak with reporters after the statement is released Wednesday afternoon, and so all the market will have to digest is the statement itself.

But the market will be looking for the Fed’s assessment of one thing in the statement: its outlook for the economy.

In a note to clients over the weekend, Bank of America’s Michael Hanson wrote that the Fed would most likely have a more “somber” outlook on the economy after a first quarter that saw economic data widely disappoint.

Hanson wrote:

At the March FOMC meeting, the Fed took any policy changes in April off the table. We don’t expect similar language about June policy at the April meeting. We do expect a more somber description of recent activity. This dovish shift in the nearterm view should translate into significantly lower odds of a June rate hike in our view. But any market participants who seek an explicit signal that June also is off the table are likely to be disappointed: the FOMC will want to maintain as much policy flexibility as possible.

During the quarter, first-quarter GDP growth was consistently revised down, and some measures like the Atlanta Fed’s GDP tracker indicates the economy may not have grown at all during the first quarter of 2015.

In a note to clients ahead of the GDP report, Joe LaVorgna at Deutsche Bank wrote: “It is possible that GDP growth (specifically productivity) is being understated, because the income side of the economy has not experienced the same degree of weakness evident in the output figures.”

Before the Fed gives its latest statement, however, it will have an answer.

Given that the Fed ruled out a rate hike in April and that Yellen will not speak with the news media after the announcement, markets have more or less been looking past the Fed meeting, or at least expecting to take it in stride with the week’s news flow. Treasury bonds, however, were selling off a bit ahead of Wednesday’s announcement, with the 10-year note rising above 2% for the first time in over a month.

Also, in addition to the big GDP number set for release Wednesday morning, the big data point for Fed policy is probably coming up Thursday with the release of the employment cost index. This report, which captures factors like employee benefits in addition to wages, is expected to show employer costs rose 0.6% in the first quarter, or 2.6% over the prior year.

Anecdotal evidence from the labor market, like the wage increases announced at Wal-Mart and Target in addition to commentary from economic surveys like the Beige Book and Monday’s Dallas Fed report, have hinted that wage pressures might be working their way through the economy. Thursday’s report will be a big test for this growing theme.

In a post ahead of Wednesday’s Fed announcement, Pimco’s Tony Crescenzi wrote that the firm still expected economic conditions would warrant a rate hike in September.

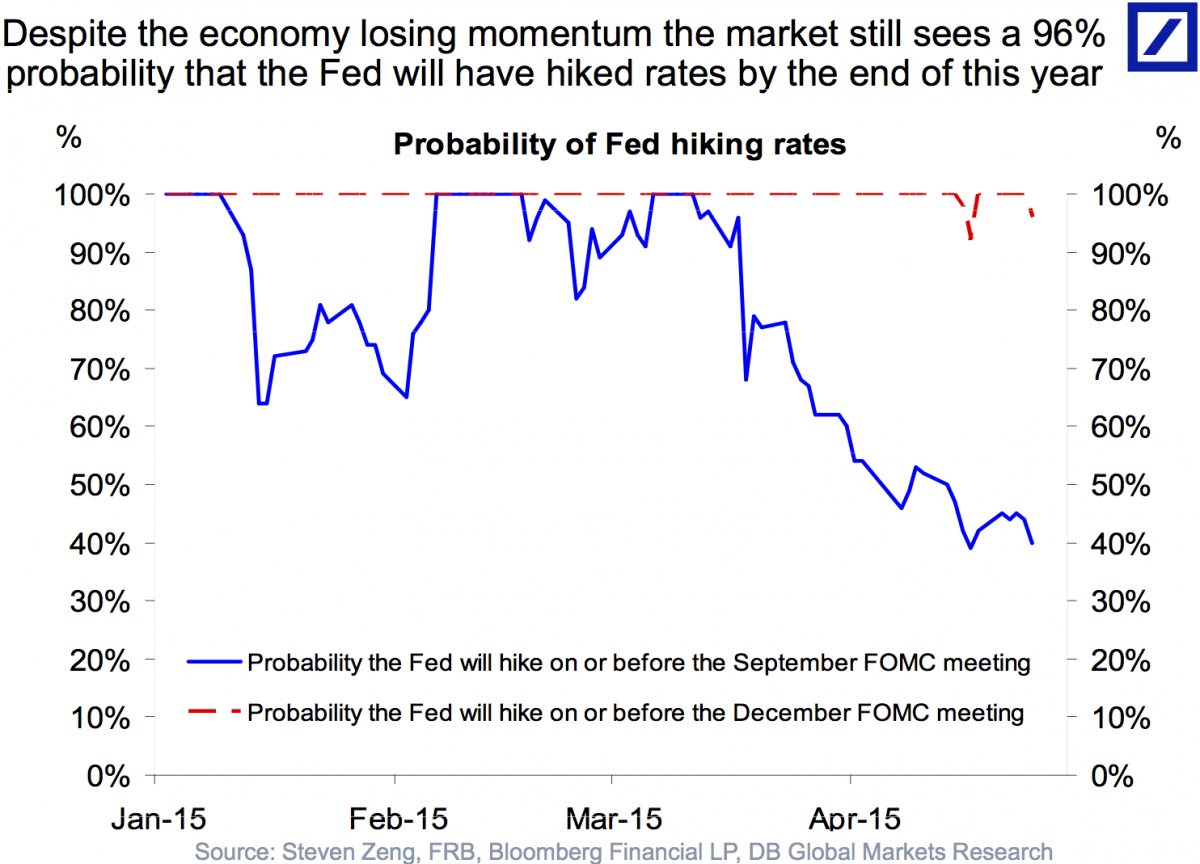

And in a chart circulated earlier this week, Deutsche Bank economist Torsten Sløk said most everyone in the market expected a rate hike by December.