Signs Of The Times

“Russia scrapped its second bond auction after the ruble’s retreat spurred bets that interest rates will increase.”

– Bloomberg, October 21.

“Russia’s international reserves shrunk for a ninth week, tumbling $7.9 billion in a little more than five months.”

– Bloomberg, October 23.

That week crude was trading at 84, nine weeks earlier it was trading at 98.

Recently it has been below 80.

“Russian tycoons seek to trim debt as [weakening] commodity demand hits values of holdings.”

– Bloomberg, October 28.

“Americans are less concerned than ever about another 1930-like Depression.”

– Rasmussen, October 23.

The numbers were that 27% thought it was “somewhat likely” and 62% polled “unlikely”. The report included that the poll was “more closely divided in 2009”.

And now for something completely honest – stupid but honest!

“Hillary: ‘Don’t Let Anybody Tell You That Businesses Create Jobs’ “

– Breitbart, October 24.

Perspective

While the stock market gets most of the attention during a boom, we all know it is not an isolated phenomenon. We have been talking about the connections to the credit markets, but the culmination of a bull market seems to be part of a universal euphoria.

On the stock side this showed up as a very low number of only 13.3% bears, the lowest since 1987. On the social side it shows up in this week’s Conference Board’s Consumer Confidence number. From 89.0 in September it soared to 94.5. This is not only a big jump, it is the highest reading since October 2007.

The low at its worst in 2009 was 39.8.

The University of Michigan’s Consumer Sentiment number for October rose from 84.6 to 86.4, which is the highest since July 2007.

The low in 2009 was around 56.

Perhaps there is a new economic law. Consumer confidence is inversely proportional to interest rates. Well, it must hold for central bankers as well.

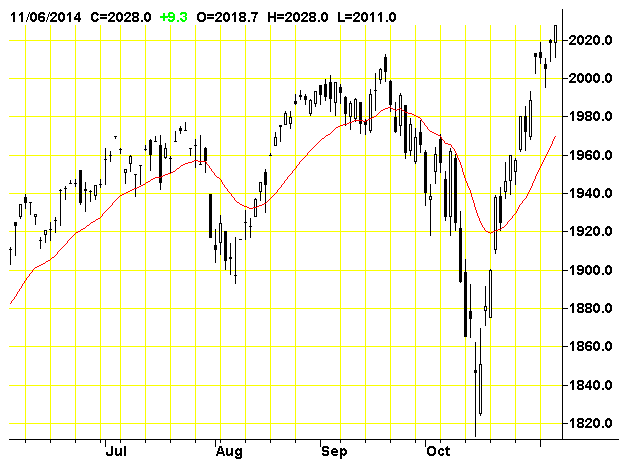

Stock Markets

Some have attributed the stock market rebound to a bullish utterance by James Bullard, a normally “hawkish” Fed employee. As interpreted by the street, the Fed was getting concerned about the severity of the correction. At less than 10%, this was severe?

This is ironical as we have never been impressed by the school of research that imagines what the Fed would do given whatever the current circumstances are. The problem with this school is that every swing in the stock market, including every irresistible transition from boom to recession has to be rationalized in FedSpeak. In the 1970s the belief was that recessions were deliberately induced to bring the rate of CPI inflation down. Well, you had to be there.

Initial selling pressure set the low for the S&P on September 16th and our ChartWorks of the next day noted the excesses on the plunge in JNK had become acute.

This prompted the relief rally and the next Pivot noted that the volatility has changed from huge Daily swings to equivalently huge Weekly swings. We have been thinking that this “Weekly” swing is getting overdone.

This has shown up in last Friday’s Inverted Springboard readings in both JNK and the S&P. As noted in Monday’s “Volatility To Resolution” piece, the sharply overbought condition seems to be leading to the expected big test in November.

The most obvious S&P targets are the lows with the last hit. These are 1860 set on the October 16th close. On the extreme it could hit 1820, which was the intra-day low. Our theme since September has been the transition from Exuberance to Divergence to Volatility to Resolution. History has made it past the first three and is working on the Resolution to another outstanding financial mania.

On the way to the Resolution, the S&P seems to be within Ross’s “ABC” rally pattern.

Credit Markets

The Inverted Springboard signal on JNK was likely to have some effect this week. The index, without interest payments, set its rebound high at 40.56. This was at the 50-Day ma and the price has slipped to 40.30. This ma was also effective on the September rebound to 40.79.

The low close on the sharp setback in June 2013 was 38.72, which looks like a reasonable target for this hit. The low close on this decline was 39.22.

Whether this will be sufficient to correct the excesses of the biggest bond bubble in history remains to be seen. At any rate we have been out of the play since the big overbought in June.

Over in Europe the excesses have also been wondrous. Understandably, as central bankers, institutions and retail have all been speculating. The ECB, in so many words, has been “pounding the table” on bonds.

This drove the yield on Greek bonds down to 5.55% in June. This broke out at 6.69% in September and in a panic soared to 8.89% in the middle of the month. The retreat was to 7.34% on the 24th and it has increased to 8.18% today. Breaking above 8.89% would have serious implications.

In the middle of the month, Russian yields broke out at 9.90% and they reached 10.22% yesterday. The post-crisis low was 6.53% set in March 2013 and the crisis high was 12.90% set in February 2009. The chart follows.

The bond future can rally on the next decline in equities.

Commodities

Many commodities have rallied out of the oversold for the stock market.

Grains (GKX) have recovered well. The low was 290 and last week we noted that if the rise got through resistance at 310, the rally could run into the spring. That was accomplished on Friday and at 320, the index is comfortably above the 50-Day ma. In getting above 325, the move could make it to the 200-Day at 355. This seems to be the best chance for a rally since January.

On base metals (GYX) we have been looking for copper to lead us down to a tradable low in November. The low for the index was 340 on the low day for the S&P and metals rallied to 358 and stopped at the 50-Day ma.

The low needs to be tested and this could be accomplished on a seasonal low sometime within the next four weeks.

Crude oil has been likely to find a seasonal low in December, but the bounce with the stock market has taken it from 78.65 to 82.51 yesterday. The next low could set up a tradable rally.

Precious Metals

This week’s slump in the sector seems tied to the rebound in stocks and low-grade bonds.

Commodities rebounded as well giving our Gold/Commodities index a needed correction.

Otherwise, gold’s real price has been rising since June and we take this as the early stages of a cyclical bull market. This will eventually drive share prices up.

When will the latter start?

We had thought that the buying opportunity would be found towards the end of this month. Last week we still thought that the time had not arrived.

The HUI has extended its decline from 251 in June to 166 today. The cyclical high was 638 in 2011. It is worth mentioning that we use momentum on the silver/gold ratio to determine important tops. In 2011 the RSI soared to 92 when we noted that level had not registered since the magnificent blow-off in January 1980. We advised that speculation had reached a “dangerous” level.

The main force on the sector has been that it has been in a cyclical bear while the orthodox world has been in a cyclical bull.

This is in transition.

Another “Rotation” in most commodities seem possible and this would help precious metal stocks.

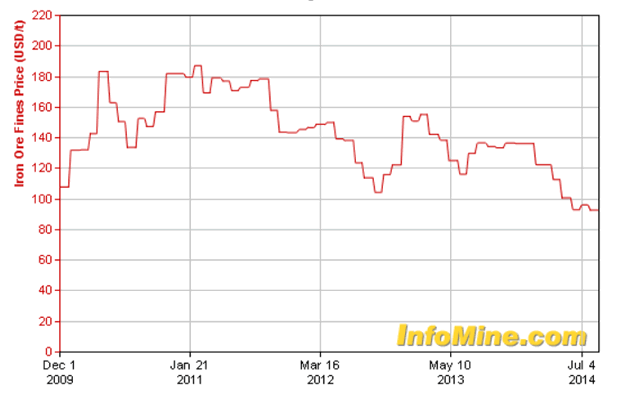

Iron Ore Prices

- The cyclical high was set in March 2011.

- This occurred with the cyclical peak in many commodities.

- Our proprietary model, the Momentum Peak Forecaster, gave a rare “Sell” that fateful April.

- The model does not provide “Buys” and it is uncertain when the general bear market will end.

Russia Ten-Year Note Yield

- Yields in Russia have been rising since the low of 6.50% in May 2013.

- Of interest is that it was a seasonal low with the rush of enthusiasm that can run into May-June.

- This was also the case with the decline from 9.52% to 8.38% in May of this year.

- This year’s breakout level was at 9.85% and that was accomplished on October 10th.

- This was a warning on most lower-grade bonds and the yield is now at 10.22%, which hasn’t been seen since 2009.

How Can Europe Service Its Debt Bubble?

Link to October 31st Bob Hoye interview on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2014/10/japan-injects-surprise-stimulus-to-world-markets