Crashing Oil Prices Portends Unspeakable Horrors

Frankly, we could write entire articles on no less than a dozen “horrible headlines” this morning, including…

- Greek stock and bonds collapsing as a 2015 default appears certain

- The collapsing French government, as Hollande has lost political support

- Plunging German growth estimates

- The growing Italian movement to secede from the Euro monetary system

- Growing support of Catalonian secession

- This morning’s horrifying plunges in U.S. Retail Sales, the Empire State Manufacturing Index and Mortgage Purchase Originations

- Wells Fargo reporting yesterday that mortgage activity has plummeted to 2008 Lehman levels

- The all-out global commodity crash, highlighted in today’s article

- Exploding currency volatility – i.e., the “single most bullish precious metals factor imaginable”

- Unmitigated Western bond yield crash as the “most damning proof yet of QE failure” exposes a collapsing global economy.

- Exploding U.S. debt about to eclipse $17.9 billion due to the “unreported” $100 billion spent on Iraq, Syria and the Ukraine

- Last night’s absurd stock repurchase admission by Intel – likely, marking the painful end of one of QE’s most hideous shareholder-destroying practices. It is estimated that 95% of all 2014 U.S. corporate earnings were plowed into buybacks – often supplemented by new debt – at historically high valuations, whilst average property, plant, and equipment averaged 22 years of age, its oldest level in 60 years.

- A new study purporting the largest “TBTF” banks may require $900 billion of capital to remain solvent

However, we don’t have time – so suffice to say, this morning’s burgeoning global market crash may well constitute the beginning of what could be a very, very rapid end. The U.S. 10-year yield closed last night at 2.21%; but as I write, is down to an astounding 1.93%, in perhaps its largest daily move ever – en route first to ZERO, and subsequently INFINITY, when the upcomingimminent (yes, I said imminent) announcement of QE’s 4, 5 and 6 emerges. Frankly, if the PPT can’t pull a rabbit out of its hat and “save” the world with unprecedented market manipulation, we think it likely the Fed will not only cancel the “taper” at its October 29th meeting but hint at reversing it entirely.

If we really get a sustained, disinflationary forecast … then I think moving back to additional asset purchases should be something we should seriously consider.

– John Williams, SF Fed President, October 14, 2014

In other words, the “countdown to the Yellen reversal” has commenced”; and if it occurs this Fall, we may well see the long-awaited collapse of the gold Cartel.

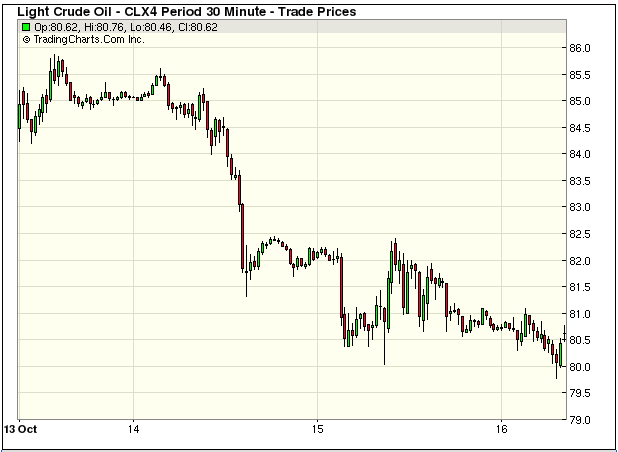

This morning (Oct 15th), WTI crude prices are down another $1+ to $81/bbl., whilst Brent Crude has plunged to $84/bbl. The carnage on energy industry equities is catastrophic, as all energy-related sectors have broken down to multi-year lows, portending a horrific 2008-style crash.

(Chart from 5:20am today)

….continue reading HERE

{kind=link}