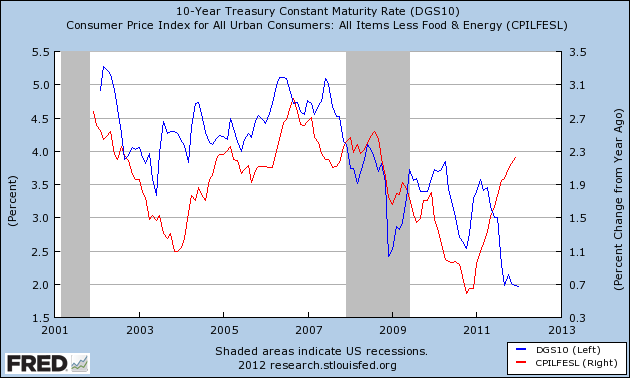

(The first powerful chart shows Interest Rates collapsing while Inflation continues to rise)

Below I show 3 charts that make the case for shorting US government bonds, specifically I’m using the 10 year Treasury. I believe that shorting US debt or 5 year+ duration is a sensible trade based on the current rate of inflation and an improving economic outlook compared to historically low Treasury yields.

1. Yields out of step with current inflation

Inflation excluding food and energy (red line – right axis) is now lower than the yield on the 10 year (blue line – left axis). Note the scales on the axis are different, but the 2 generally move together, and inflation is currently 30 bps higher than the 10 year yield. This suggests either falling inflation or an increase in yields, because it is unlikely investors will accept negative real returns on bonds for long.

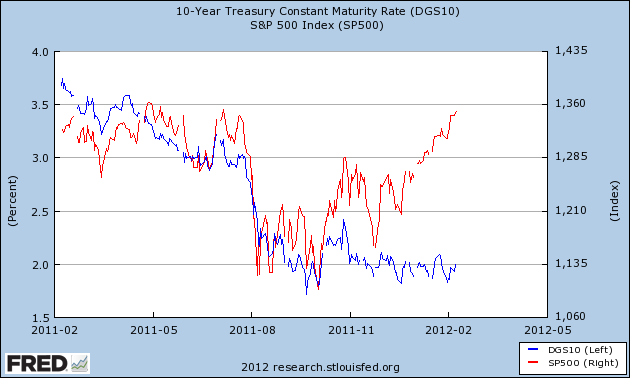

2. Disconnect between the S&P and bonds

Since late 2011, the S&P 500 (red line) has risen significantly, whereas bond yields (blue line) have remained flat. It is likely that either the stock market or bonds will decline to correct this.

3. Declining dollar may drive domestic inflation

The dollar shown below on a trade-weighted basis, is flat to declining, this matters because the exchange rate determines the relative price of domestic goods vs. imports. As the dollar falls, domestic goods become relatively cheaper, raising demand for domestic goods. More money causing the same amount of goods is generally considered inflationary. Of course, one way for the dollar to strength is for yields on US debt to rise.

A lot of this thinking is predicated on continued economic recovery through 2012 into 2013. If that were to change, perhaps if Europe’s decline deepens, many of the relationships above would unravel. I am highlighting imbalances which can be brought back into balance from either side i.e. bonds could fall OR alternatively the S&P could fall back and inflation could fall too (which is pretty much what one would expect if the economy loses steam).

In addition, the value of bonds are their diversification from equities, in shorting treasuries you are giving up that hedge and if the stock market falls, a short treasury bet would likely decline with it providing no diversification benefit. Of course, we should also not ignore the Fed and Operation Twist, which is looking to aggressively lower yields on longer term debt, however there comes a point where the Fed’s desire to lower longer term rates is overtaken by economic trends, just as the Fed cannot directly set the exchange rate.

Let me leave you with one final point, the average inflation rate in the US from 1914-2010 has been 3.4% with the current 10 year yield at 2%, we are, broadly speaking, forecasting inflation to be below average for the next 10 years. That’s not to say it can’t happen – deflation has happened before, but it’s against the run of the long-term trend.

Operationalizing the trade

This is not the easiest trade to implement and certainly not for the risk averse. Though there are plenty of inverse bond ETFs and ETNs, I am personally a little sceptical of them given short track records and relatively high fees. Personally, I prefer to short the larger more liquid bond ETFs directly, such as TLT.

Disclosure: I am short TLT.