· The Obama administration said on Thursday that it had “serious concerns” about the value of the renminbi, but stopped short of accusing China of manipulating its currency in a closely watched report to Congress. (FT)

· Key Reports today:

Treasury International Capital Data (or are they still buying the Treasuries)

Quotable

![]() Horatio:

Horatio:

He waxes desperate with imagination.

Marcellus:

Let’s follow. ‘Tis not fit thus to obey him.

Horatio:

Have after. To what issue will this come?

Marcellus:

Something is rotten in the state of Denmark.

Horatio:

Heaven will direct it.

Marcellus:

Nay, let’s follow him. [Exeunt.]

![]() FX Trading – Weak dollar good or bad…depends on your time frame I guess

FX Trading – Weak dollar good or bad…depends on your time frame I guess

Richard Berner is an economist from Morgan Stanley—I think he is very good. He made these comments in a research note recently regarding the US dollar [our emphasis]:

“The dollar’s recent slide is only reversing a substantial rise that began in mid-2008; on a broad, trade-weighted basis the dollar is actually 8% stronger than it was at that time and now stands about where it was two years ago. Moreover, the depreciation has been orderly and has been accompanied by falling, not rising, risk premiums. And one key driver – the US current account deficit, which is a measure of US external financing needs – has shrunk to less than 3% of GDP, or half its peak value.

“Disinflationary forces dominate inflation for now. There is broad agreement that a weaker dollar can contribute to higher inflation, both through its direct influence on import and commodity prices and via its indirect impact on inflation expectations. The interplay among them is important: While a weaker dollar and rising commodity prices will primarily change relative prices, like those of imports and energy goods and services, they can nonetheless influence both inflation expectations and inflation itself.

“In our view, a weaker dollar and rising commodity prices are tangible evidence of the Fed’s reflationary thrust. Since the Fed stepped up its quantitative easing at the March 18 FOMC meeting, the dollar has declined on a broad, trade-weighted basis by 8.7%, crude oil quotes have jumped by 46%, and broad commodity price indexes have risen by 18-26%. To be sure, the dollar’s recent decline reflects greatly reduced risk-aversion, and rising commodity prices also are a sign of investors’ increased appetite for risk amid hopes for global recovery. But they are all part of the policy transmission process. Although exchange rate ‘pass-through’ has weakened in recent years, it isn’t zero. A weaker dollar will help to limit inflation downside through import prices, commodity prices and inflation expectations.”

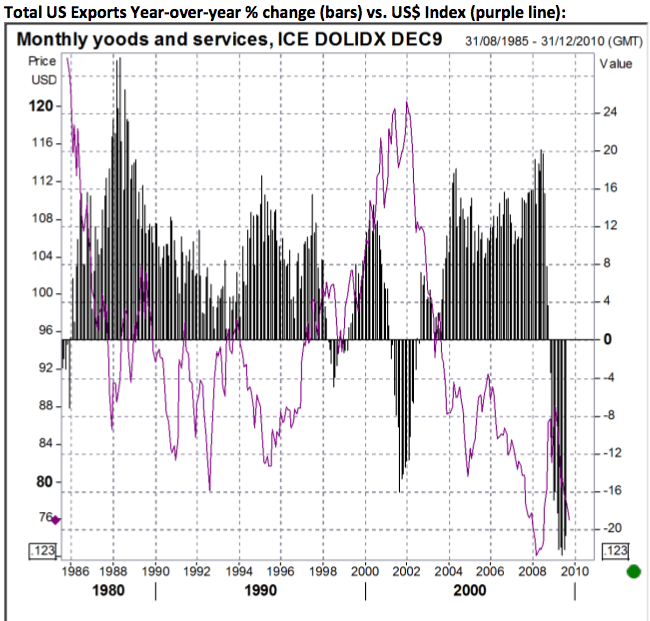

Mr. Berner is of the view that a weak dollar does significantly help US exports, with an admitted lag. We don’t deny there is benefit on the export front from a weakening dollar…as the chart tends to support that view….

Total US Exports Year-over-year % change (bars) vs. US$ Index (purple line):

There will be cyclical bounces higher along the way for the dollar, as the US economic growth relative to its competitors recovers and US interest rates rise. But we are concerned until there is a major policy shift, which has capital formation at its core, the dollar will continue to fade as the US dollar index continues the long-term pattern of lower highs and lower lows despite any cyclical rebound in exports thanks to lower US goods prices.

Today, the dollar is bouncing higher against the pack. Have the fundamentals changed? Not really. Three factors we see in play at the moment:

1) Negative dollar sentiment extreme and technically extended

2) Concern of correction in the stock market, which may lead to a strong dollar bounce if correlations hold

3) Though minor, a bit of fear the Fed may put some risk back into the one-way dollar bet

Three guesses indeed. But why we decided to take some profit on our short USD-Norwegian Krone position yesterday, and add long USDJPY long (JY futures short).

Stay tuned.

Jack Crooks

Black Swan Capital

Triffin’s Dilemma and why the dollar is in long-term trouble?

David here …

Jack and JR are putting the finishing touches on our monthly Currency ETF Investor newsletter, which will be sent to our subscribers today. And I think this month’s topic is interesting and timely, given the concern we all have about the potential for long-term decline in the US dollar and loss of the dollar’s world reserve currency status.

If this is an area of interest to you too, and you’d like to see our latest recommendations to take best advantage of the dollar trend with the ease of exchange traded fund investing, I urge you to subscribe to our Currency ETF Investor HERE.

For $39 per year I doubt you will find a better bargain for you potential return anywhere else.

Remember, your subscription comes with a 30-day risk-free money back guarantee, no questions asked, if you determine it’s not the right fit for you.

Thanks for reading,

David Newman

Black Swan Capital LLC

P.S. If you might be interesting in our more aggressive forex and currency futures trading service, please send me an email at info@blackswantrading.com for information, or you can subscribe at our website. Jack and JR are finding some excellent trade setups lately.