This summary from ZeroHedge.com whose founder Tyler Durden is possessed of the belief that a return to (more) efficient markets is a possibility and a necessity. Refugee of various asset managers and advisers, as his namesake, Tyler remains convinced the current model is flawed and a deleveraging at every level of modern society is needed to reignite the fundamental entrepreneurial spirit.

Interest Rate Observations From Morgan Stanley

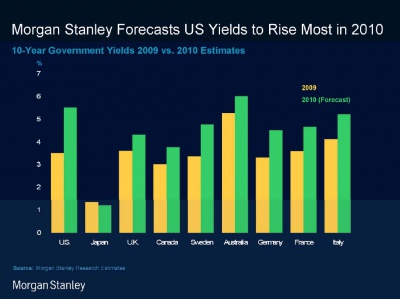

Morgan Stanley, which recently made the daring call for a 5.5% yield on the 10 year by the end of 2010, and which has recently caught the attention of many finance pundits, provides some more projections for 10 year rates not only in the US but globally. Curiously, out of all countries, Morgan Stanley only sees Japan lower by the end of 2010, with all developed countries higher, but none moving as much as the US. Furthermore, by the end of 2010, only Australia will sport a 10 year rate wider than the US, predicts MS.

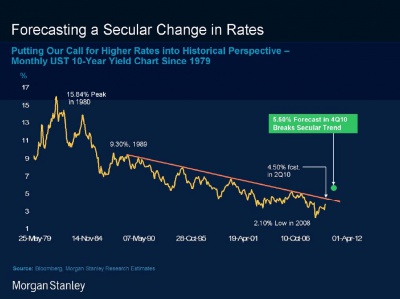

The recent evolution of the credit market in the US is seen on the next slide: if indeed the 10 year hits 5.5% this will be the first major break of the secular trendline ever tighter since the 1980’s bull market. Can someone make the case that all a key reason for secular market gains over the past 30 years have been on the back of a consistently lowering cost of debt capital? We think the answer is a resounding yes.

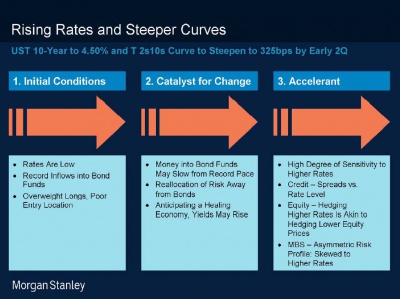

The last observation highlights the expectation that the 2s10s curve will steepen to a record 325 bps by early Q2. Whether this happens as quickly as expected will depend on the presence of an “accelerant” which MS defines as the following:

- High degree of sensitivity to higher rates

- Spreads versus Rate levels from a credit perspective

- Hedging higher rates is comparable to hedging lower equity prices from an equity perspective

- Asymmewtric risk profile in MBS which is skewed to higher rates.

(Larger Image of the Chart below HERE. )

What is missing are the implications for the economy if MS is indeed right. But those are all too obvious, which is why the Fed will do everything in its power to prevent that from happening.