1. THE PRECIOUS METALS TUG OF WAR

When I get to the bottom

I go back to the top of the slide

Where I stop and turn

and I go for a ride … – Paul McCartney, 1968

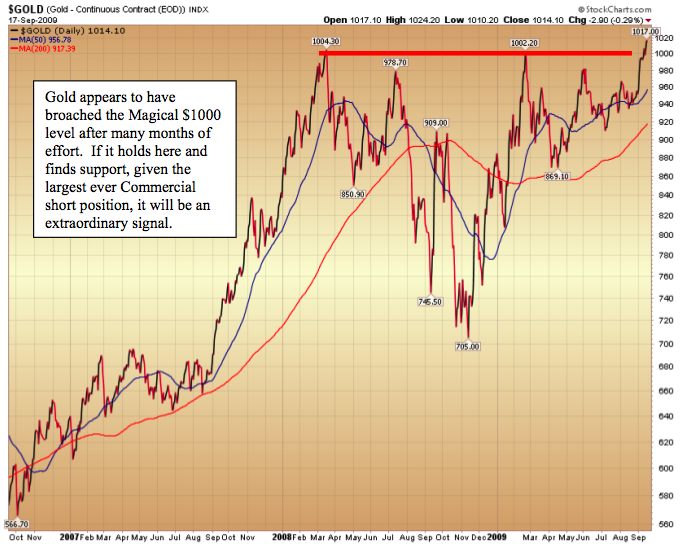

As if on the playground slide, so aptly described 40 years ago by the Beatles Paul McCartney, gold and silver buyers and the commercial shorts are now locked in a struggle that will reveal whether we shall inflate out of our economic misery or whether deflation headwinds shall continue to constrain the US and most economies globally. For the past 18 months gold and silver prices have vacillated around $1000 and $14 respectively. There are many cross currents in this struggle. The outcome is uncertain in the short run. If gold holds above the $1000 per ounce level and silver above $17 we shall have our answer shortly.

Cross currents? First and foremost, the US Federal Reserve wants inflation. There is no more important philosophical foundation of the Bernanke Fed than “inflation targeting.” The belief in the Washington DC fishbowl, indeed most central bank boardrooms, is that inflation is the lesser of the two evils. An omniscient and independent Federal Reserve Bank has the necessary tools, according to monetary policy makers, to control this lesser evil. The Fed believes that deflation, once in control, will run its own price destroying course to exhaustion and then renewal. This seems to be anathema to Central Bankers.

But there is another major actor in this arms race. The grandiose fiscal plans of the Obama Administration and the Congress will have an impact. Even Warren Buffet who supported the new president recently noted,

“This fiscal year, though, the deficit will rise to about 13 percent of G.D.P., more than twice the non-wartime record. In dollars, that equates to a staggering $1.8 trillion. Fiscally, we are in uncharted territory.”

With current spending plans, net debt will increase to 56% of GDP leaving the US government no choice but to print (might I use the word, “invent”?) money – a lot of money. Mr. Buffet reckons that even if Americans saved $500 billion, Congress and the Administration would be forced to “find” another $900 billion. Under these circumstances and with $1 trillion in health care reform on the way, a much larger inflation fire will be lit.

Then, of course, we have China and India and perhaps the rest of the newly emerging world. China’s policy is to permit the purchase of silver in up to 5 kilogram bars by its citizens recently. So we come to the key point in the rapidly expanding drama. Chinese banks are requesting their gold, now stored in London, be returned to Hong Kong there to be safeguarded – an unusual move but one we think presages a new Asian gold repository for Asian Central bankers chastened by the recent turmoil in the West.

Will the commercial shorts in gold and silver be overrun? It has never happened in the past. Many investment bankers, viewing the extraordinarily high levels of investors long the gold and silver futures, are predicting a dramatic pullback in both gold and silver prices. They are warning investors to take profits. The commercial shorts have always reigned in the gold and silver spot markets in the past. One thing we are quite sure of – there is not enough physical gold and silver to cover the massive commercial short positions. At present gold producer Barrick is attempting to cover its naked hedges (shorts) and finding the going rough. Even if Barrick committed all its gold production for a year it would still fall far short of covering its hedge positions. In short, Barrick is naked.

Given these competing cross-currents and the longer term necessity / inevitability of inflation we think that the commercial shorts will in fact be forced to cover. We are just not certain when that covering might occur. Obviously the commercials do not see this

eventuality the way we do – even as Barrick executives are trying to cover their shorts in some degree of panic.

Perhaps the much beloved and at the same time reviled John Maynard Keynes said it best in his seminal work, The Economic Consequences of the Peace following World War I in

1920.

“But who can say how much is endurable, or in what direction men will seek at last to escape from their misfortunes?”

“Thus the menace of inflationism described above is not merely a product of the war, of

which peace begins the cure. It is a continuing phenomenon of which the end is not yet in

sight.”

Is inflation ever a palatable solution? At present it seems to be the desired and most likely scenario for the US economy. The alternative, deflation, is quite out of the question. Yes Dear Discovery Investor gold is going much higher – it is just a matter of time.

You can sign up for Dr. Berry’s free Morning Notes HERE.

Michael Berry has been a portfolio manager for both Heartland Advisors and Kemper Scudder where he successfully managed small and mid cap value portfolios. Dr. Berry has specialized in the study of behavioral strategies for investing and has been published in a number of academic and practitioner journals. His definitive work on earnings surprise, with David Dreman, was published in 1995 in the Financial Analysts Journal.

Previously, Dr. Berry was a professor of investments at the Colgate Darden Graduate School of Business Administration at the University of Virginia and has also held the Wheat First Endowed Chair at James Madison University.

Dr. Berry is a respected and dynamic speaker. He regularly presents around the world on topics such as value investing, the role of Austrian Economics in investment management, behavioral investing strategies and is a specialist in developing case studies to teach investors how to invest. While a professor, he published a case book, Managing Investments: A Case Approach.

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition Dr. Berry may review investments that are not registered in the U.S. He owns shares and in Goldcorp, Senesco Technologies, Natural Blue, Horseshoe Gold, Derek Oil and Gas, Terraco Gold, Neuralstem, Piedmont Mining, MegaWest Energy, Valcent Products, CGX Energy, MacMillan Gold and Quaterra Resources. He has been awarded 250,000 options on Terraco Gold exercisable at C$.20 for 2 years, forattest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.