I am back from the Forbes cruise to Mexico and starting to deal with a thousand things, but first on the list is making sure you get this week’s Outside the Box. And a good one it is. In fact, it is two short pieces coming to us from friends based in London over the pond.

Both of them have to deal with the unfolding crisis that is Europe, which is going to unfold for several years as they lurch from solution to solution. The first is from Dylan Grice of Societe Generale and reminds us why we should put no stock in what leaders say about a crisis. He has lined up the statements of leaders from one crisis after another. He finds a simple, repeating pattern. And shows where we are now.

The second is from hedge fund manager Omar Sayed, who I met last time I was sin London. A very bright chap and good guy. He offers us very succinctly four paths that Europe can take. Some of them are not pretty. It all makes for a very interesting OTB. I trust your week will go well.

Your over-dosed on guacamole (and it was worth it) analyst,

John Mauldin, Editor

Outside the Box

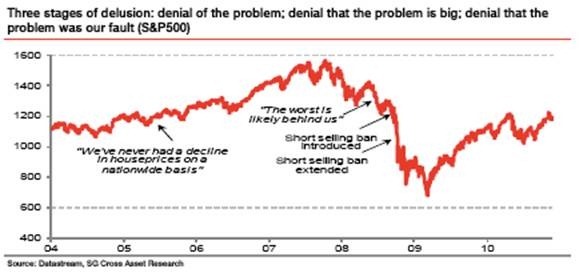

The Three Stages of Delusion

The recent sequence of reassurances from various eurozone policymakers suggests we are in the early, not latter, stages of the euro crisis. Only an Anglo-Saxon style QE will prevent dissolution of the euro. Such a radically un-German solution will only be taken with a full acceptance of how serious the euro’s problems are. But denial persists.

The dawning of reality hurts. Prodded and bullied along a tortuous emotional path by events unforeseen and beyond our control, we descend through three phases: the first is denial that there is a problem; the second is denial that there is a big problem; the third is denial that the problem was anything to do with us.

US policymakers’ three steps during the housing crash fit the template well. Asked in 2005 about the danger posed to the economy by the housing bubble, Bernanke responded: “I guess I don’t buy your premise. It’s a pretty unlikely possibility. We’ve never had a decline in house prices on a nationwide basis.” Here was the denial that there was a problem. But as sub-prime issues arose, Ben Bernanke reassured the world that they would be “contained.” And when Bear Stearns collapsed, Hank Paulson promised “The worst is likely to be behind us.” Here was denial that there was a big problem.

Soon the financial system was on the brink of collapse. There could no longer be any credible denial of the problem, so the locus of delusions shifted: there was a problem, but it was someone else’s fault. Thus a ban on naked short selling of financials was implemented in Sept/Oct 2008, as though the crisis was somehow short-sellers’ fault. (It certainly wasn’t the Fed’s fault, according to the Fed. Ben Bernanke argued this year “Economists … have found that only a small portion of the increase in house prices … can be attributed to the stance of US monetary policy.”)

What’s interesting is that the journey Bernanke and Co. took fits the journeys of policymakers presiding over crises past very closely, as I’ll show inside. What’s worrying is that taken in this context, eurozone policymakers’ denials/reassurances sound eerily familiar. And if these past crises are any guide, the euro crisis is still in its early stages.

A descent through the three stages of delusion characterises most crises. Dick Fuld went from saying “as long as I live, Lehman will never be sold” in December 2007, to “We have access to Fed funds; we can’t fail now” during the summer of 2008, to agreeing with a colleague that half of any capital injection then being negotiated with the Korean Development Bank be used to buy back Lehman stock, to “hurt Einhorn bad.”

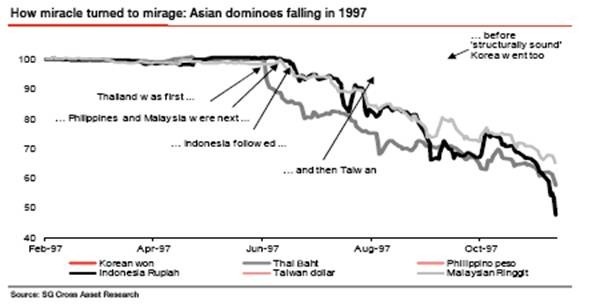

Identical stages can be traced during the Asian Crisis of 1997. For those who don’t recall, the Asian Tigers were ‘miracle’economies whose dizzying growth rates proved the superiority of export liberalisation, high investment and free markets. Their miracle image was burnished by the ‘good crisis’ they enjoyed in 1994, when their fixed exchange rate systems (they were pegged to the dollar) successfully withstood the contagion caused by the collapse of the Mexican peso.

Bear in mind that the world had bought into the Asian Tiger story hook, line, and sinker. The World Bank wrote a now infamous series of reports called “The East Asian Miracle” from 1993, lauding the strength of the region’s institutions and preaching its commitment to an export-driven growth model to anyone who’d listen. And while there was a feeling that some tigers (e.g. Thailand and the Philippines) were riskier than others (Indonesia), the idea that Taiwan or South Korea would be caught up in anything was viewed as utterly preposterous. Early in 1997, Jeffrey Sachs said:

“Since the economic structure of Korea is fundamentally different from that of Mexico, there is no possibility of recurrence of the situation that happened to Mexico.”

But early in 1997, problems emerged. The first sign of trouble came in Korea in January when a large chaebol called Hanbo Steel collapsed under $6bn of debts. Then in February, Thai property company Somprasong Land missed a payment on foreign debt in February. These turned out to be the first cockroaches. The following chart shows the sequence of events which would soon follow. First the small economies fell – then the big ones.

Yet denial that there was any problem characterized early observations. Immediately following the Thai government’s $3.9bn aid to Thai banks to cover dud property loans, Michel Camdessus – then head of the IMF – said, “I don’t see any reason for this crisis to develop further.” And on 30th June that year, Chavalit Yongchaiyudh, then Thai Prime Minister, made a televised address to the nation saying “We will never devalue the baht.”

Yet the baht was floated on 2 July. It was soon followed by the Philippine peso.

But the initial denial that there was a problem simply became denial that there was a big problem. Indonesia wasn’t Thailand, after all. According to an article in the 8th Oct 1997 New York Times:

“Indonesia’s financial condition is far better than Thailand’s was this summer … while Thailand depleted its foreign-currency reserves in a last-ditch effort to prop up its currency, the baht, Indonesia still holds foreign reserves of about $27 billion.”

And as the Indonesian crisis began to intensify and the US made financial help available as a precaution, an Administration official said: “We don’t expect that Indonesia will need to draw on our direct help, but what we need to address here is an atmosphere of contagion.”

As it turned out, Indonesia wasn’t Thailand. It was worse. It would prove to be the worst affected of the Asian tigers with a near 80% exchange rate collapse bankrupting the corporate sector which had borrowed heavily in dollars. GDP collapsed by 14%, triggering unrest and street violence which ultimately forced out President Suharto.

Yet denial that there was a big problem persisted. James Wolfensohn, then president of the World Bank, reassured that the Indonesian bailout marked the end of the crisis: “The worst is over” he proclaimed confidently.

Korea wasn’t Indonesia. Michel Camdessus, said on Nov 6th: “I don’t believe that the situation in South Korea is as alarming as the one in Indonesia a couple of weeks ago.” Yet South Korea turned out to be just as vulnerable, and certainly more costly. On December 1st 1997, the government said it had agreed to a $55bn bail-out (which then, was the largest bailout in the history of the world. In today’s money it’s a mere $75bn, less than the bill for Ireland). The storm moved on. Before petering out it would engulf Latin America, then Russia, and then the once mighty hedge fund LTCM. But for now, Asia had been destroyed. The miracle was myth. The depth of the problems was now undeniable.

Yet the denial persisted, only now it emphasised the fault of others to demonstrate that the crisis was in no way related to anything policymakers had done. It was all caused by speculators, international bankers and the foreign media. Most infamous was Malaysia’s then Prime Minister Mahathir Mohamed blaming George Soros, who he bizarrely implied was part of some kind of wider plot. “Today we have seen how easily foreigners deliberately bring down our economy by undermining our currency and stock exchange …” and “Soros is part of a worldwide Jewish conspiracy.”

There’s nothing unusual about the emotional need to find a scapegoat when things go wrong. As always, Shakespeare wrote about it four centuries ago. From King Lear:

“This is the excellent foppery of the world, that, when we are sick in fortune – often the surfeit of our own behaviour – we make guilty of our disasters the sun, the moon, and the stars: as if we were villains by necessity; fools by heavenly compulsion; knaves, thieves, and treachers by spherical predominance; drunkards, liars, and adulterers, by an enforced obedience of planetary influence; and all that we are evil in, by a divine thrusting on: an admirable evasion of whoremaster man, to lay his goatish disposition to the charge of a star!”

And if we’re looking for signposts on the way to a crisis’ closing chapters, it turns out that the “excellent foppery” of blaming everyone else is a good indication. Thus, as the Greek crisis unfolded in December 2009, George Papandreou went from denial of the problem, insisting it to be “out of the question” that Greece would resort to the IMF, to denial that it was the Greeks’ fault, lamenting in March 2010 that “we ourselves were in the last few months the victims of speculators.”

As the Irish crisis reached its conclusion, Finance Minister Brian Lenihan blamed the “unintended consequences” of various German and French comments for its spiralling borrowing costs.

Today Spain is the battlefield. A few weeks ago, the Spanish were in denial that there was a problem. Zapatero said “I believe that the debt crisis affecting Spain, and the eurozone in general, has passed.” Now they are in denial that there is a big problem. Last week, Spanish Finance Minister Elena Salgado said there was “absolutely no risk” the country would need an international bailout and stressed the differences between Spain and Ireland, much as the Indonesians stressed the difference between themselves and the Thais thirteen years ago:

“Our financial sector has always had the Bank of Spain’s supervision and regulation, which is what has probably been missing in Ireland … We have a solid financial sector and we should remember that it’s the financial sector that’s provoking the difficult situation in Ireland.”

When they start blaming everyone else for their problems, we’ll know their crisis is nearly over Until then, their plight likely has some way to go.

But of course, the real issue isn’t Ireland, or Portugal or even Spain. The real crisis is the euro, and the strains continued membership is placing on the relationships between euro members and the attitude of electorates in the member states towards the single currency.

Yet policymakers are as in as much denial that there is a big problem (i.e. with the euro rather than any individual country) as Ben Bernanke and Hank Paulson were that there was a housing bust, as Dick Fuld was that Lehman was toast, or as the IMF was that Thailand, let alone Asia, had profound economic weaknesses. Last week the Finnish Central Bank head and ECB Governor Erkki Liikanen said “The euro will survive. It is not questioned.” Klaus Regling, heading up the EFSF, said “No country will give up the euro of its own will: for weaker countries that would be economic suicide, likewise for the stronger countries. And politically Europe would only have half the value without the euro.”

Such logic has been used before. Barry Eichengreen wrote in 2007 that euro membership was effectively irreversible because withdrawal would be too traumatic. But what if the cost of staying in the euro becomes so high that exit is preferable? Surely this is the risk in Germany’s current strategy.

Peripheral eurozone countries need to default. Traditionally this is done with currency debasement (which the Fed and the BoE have already begun) or by imposing a haircut on lenders. Germany refuses to sanction the former, while flagging up the latter triggered the latest bout of contagion. Instead, they are imposing depressions on countries which lose the bond market’s confidence.

How many years of austerity before the voters of Greece/Ireland/Spain/wherever blame Germany, France, or the euro for everything that is wrong with their economy? Will this become the blame game signalling the final chapter of the euro’s crisis?

I certainly hope not. Last week, Axel Weber said: “The European Financial Stability Fund should be sufficient to dissuade markets from speculating against the solvency of Eurozone member countries, and if not, more money will be provided.”

If and only if that money comes from the ECB’s printing presses – in the style of the BoE and the Fed – will Mr. Weber be correct. A large risk rally will ensue. If not, we still have a long, long way to go. On 27 May this year, following the original set-up of the EFSF, I wrote:

“The EU’s ‘shock and awe’ $1trillion rescue was certainly a big number and reflected European governments going all in. But going all in is risky if you don’t have a strong hand, and the EU’s seems weak. Two-thirds of the rescue money comes from the EU itself, which means that the distressed eurozone borrowers are to be saved by more borrowing by … er … the distressed eurozone borrowers.”

This remains the case. The EFSF is flawed. It invites speculative attack. Simply expanding it in its current form so that the ‘solvent core’ commits to raise yet more funds for the ‘insolvent periphery’ fails to address the risk that as more dominos fall the bailers shrink relative to the bailees (Italy and Spain combined – who’s spreads have been blowing out this week – are combined bigger than Germany). At what point does the insolvent periphery include so many countries that markets lose confidence in the solvency of the shrinking core to bail them out. Leaving aside for now the unpleasant reality that the solvent core might not actually be so solvent, perhaps the spread between ‘insolvent’ Greece and solvent France should be narrower? I wish I knew. In the absence of ECB printing, I suspect we’re going to find out.

John F. Mauldin

johnmauldin@investorsinsight.com

Sign up for a Free subscription for Outside the Box HERE