Midnight Candles

A cold wind from the future blows into my nighttime bedroom, more often than not during those midnight hours when fear dominates and hope retreats to a netherworld. This wind is a spectre, an oracle of darkness and eventual death, not easily dismissed. Once merely a whisper, its decibels intensify with the advancing years. It will be heard, this reaper – this grim reaper, yet in the nights when it howls the loudest I fight back, silently screaming for it to get out, to leave me alone, to let it all be a bad dream. It never is. Shakespeare’s Macbeth expressed it more subtly: “Out, out, brief candle!” Yet the finer words provide no solace; the final act is always the same.

Those of you in your sixties and older know of what I speak; even during daylight hours you read the obits and notice that contemporaries have passed into the beyond. Those of you much younger must wonder what has come over me, yet I was young once too. I remember as a teenager camping out under the stars with friends wondering aloud at the mystery of it all, knowing the reaper was far off in the distance, so far away that death was more a philosophical discussion point than an impending reality. In my thirties, I recall standing in front of a mirror in my physical prime and instructing my image that I would never grow old, that I somehow would live forever, that I, the me, the ego, would be eternal. Now when I face the glass my eyes avoid the unmistakable conclusion: I am everyman – everyone that ever was and ever will be. This world will outlast me.

What to do? Enjoy these senior years and take advantage of the gifts I have been given – a healthy 65-year-old body, an amazing job where I can still make a vital contribution, a wonderful wife who shines brightly and muffles the sound of my nighttime intruder. Still there is no acceptance of Macbeth’s or any of our “dusty deaths.” At midnight there is only fear and rage – rage against this night whose wind will one day take us all.

An investment segue is a tough one this month: markets whistling past the graveyard? A vampire economy? A ghostly correction ahead? Pretty lame, so I’ll jump straight into a discussion of why in a New Normal economy (1) almost all assets appear to be overvalued on a long-term basis, and, therefore, (2) policymakers need to maintain artificially low interest rates and supportive easing measures in order to keep economies on the “right side of the grass.”

Let me start out by summarizing a long-standing PIMCO thesis: The U.S. and most other G-7 economies have been significantly and artificially influenced by asset price appreciation for decades. Stock and home prices went up – then consumers liquefied and spent the capital gains either by borrowing against them or selling outright. Growth, in other words, was influenced on the upside by leverage, securitization, and the belief that wealth creation was a function of asset appreciation as opposed to the production of goods and services. American and other similarly addicted global citizens long ago learned to focus on markets as opposed to the economic foundation behind them. How many TV shots have you seen of people on the Times Square Jumbotron applauding the announcement of the latest GDP growth numbers or job creation? None, of course, but we see daily opening and closing market crescendos of jubilant capitalists on the NYSE and NASDAQ cheering the movement of markets – either up or down. My point: Asset prices are embedded not only in our psyche, but the actual growth rate of our economy. If they don’t go up – economies don’t do well, and when they go down, the economy can be horrid.

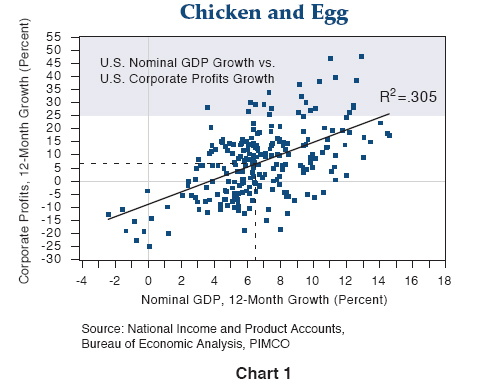

To some this might seem like a chicken and egg conundrum because they naturally move together. For the most part they do – and should. As pointed out in a recent New York Times article titled “Dow Bubble?,” stocks and nominal GDP growth should be correlated because profits and nominal GDP are correlated as well. Witness the PIMCO Chart 1, researched by Saumil Parikh, which covers a time period of 50 years. Granted the R2 correlation is only .305, but that is to be expected – profits are also a function of the respective entities that feed at the GDP growth trough – corporations, labor, government and other countries – and when corporations and their profits are ascendant they do well; when not, they fall below the best fit line appearing in the chart. Notice as well that in a normally functioning economy growing at 6-7% nominal GDP, that profits grow at the same rate. (At growth distribution tails there are substantial distortions.) And if long term profits match nominal GDP growth then theoretically stock prices should too.

Not so. What has happened is that our “paper asset” economy has driven not only stock prices, but all asset prices higher than the economic growth required to justify them. Granted, one must be careful of beginning and ending data points in any theoretical “proof.” Such is the fallacy of Jeremy Siegel’s Stocks for the Long Run approach which begins at very low PEs and ends most long-term time periods with much higher ones, justifying a 6.5% “Siegel constant” real rate of return for U.S. equities over the past 75 years or so. It may also be a weakness of the New York Times “Dow Bubble” article where the authors claim that since the Dow Jones average was at 4,000 in 1995, that a 100% step-for-step correlation with nominal GDP growth since then would produce a reasonable valuation of 7,800 – not the current 10,000.

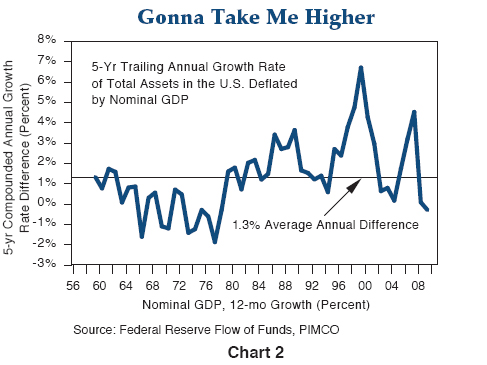

Having said that, let me introduce Chart 2 a PIMCO long-term (half-century) chart comparing the annual percentage growth rate of a much broader category of assets than stocks alone relative to nominal GDP. Let’s not just make this a stock market roast, let’s extend it to bonds, commercial real estate, and anything that has a price tag on it to see if those price stickers are justified by historical growth in the economy.

This comparison uses a different format with a smoothing five-year trailing valuation growth rate for all U.S. assets since 1956 vs. corresponding economic growth. Several interesting points. First of all, assets didn’t always appreciate faster than GDP. For the first several decades of this history, economic growth, not paper wealth, was king. We were getting richer by making things, not paper. Beginning in the 1980s, however, the cult of the markets, which included the development of financial derivatives and the increasing use of leverage, began to dominate. A long history marred only by negative givebacks during recessions in the early 1990s, 2001–2002, and 2008–2009, produced a persistent increase in asset prices vs. nominal GDP that led to an average overall 50-year appreciation advantage of 1.3% annually. That’s another way of saying you would have been far better off investing in paper than factories or machinery or the requisite components of an educated workforce. We, in effect, were hollowing out our productive future at the expense of worthless paper such as subprimes, dotcoms, or in part, blue chip stocks and investment grade/government bonds. Putting a compounding computer to this 1.3% annual outperformance for 50 years, produces a double, and leads to the conclusion that the return from all assets was 100% (or 15 trillion – one year’s GDP) higher than what it theoretically should have been. Financial leverage, in other words, drove the prices of stocks, bonds, homes, and shopping malls to extraordinary valuation levels – at least compared to 1956 – and there could be payback ahead as the leveraging turns into delevering and nominal GDP growth regains the winner’s platform.

This 100% overvaluation from recent price peaks of course is crude, simplistic, and unrealistically pessimistic. It implies that stocks should be at – gasp – Dow 7,000 – and that home prices – gasp – should be cut in half from 2007 levels, and that commercial real estate (Las Vegas hotels, big city office buildings that are 20% empty) should likewise face the delevering guillotine. Some of these price adjustments have already taken place, and to be fair, corporate and high yield bonds as well, should be thrown into this overpriced vortex more resemblant of a black hole than American-style paper wealth capitalism. This is where it gets tricky, however, because policymakers, (The Fed, the Treasury, the FDIC) recognize the predicament, maybe not with the same model or in the same magnitude, but they recognize that asset prices must be supported in order to generate positive future nominal GDP growth somewhere close to historical norms. The virus has infected far too many parts of the economy’s body, for far too long, to go cold turkey. The Japanese example over the past 15 years is an excellent historical reference point. Their quantitative easing and near-0% short-term interest rates eventually arrested equity and property market deflation but at much greater percentage losses, which produced an economy barely above the grass as opposed to buried six feet under. The current objective of global policymakers is to do likewise – keep the capitalistic patient alive through asset price support, but at an “old normal” pace if possible, six feet or 6% in U.S. nominal GDP terms above the grass.

That support, of course, comes in numerous ways. Financial system guarantees, TARP recapitalization of banks, TAFs, TALFs, PPIFs – and in Europe and the UK, low interest rate term financing, semi-bank nationalizations, and asset purchase programs similar to the United States. In the case of the U.S., the amount of the implicit and explicit financial support given by policymakers totals perhaps as much as $5 trillion, which goes part way to support the $15 trillion overvaluation of assets theoretically calculated in the PIMCO model (100% of nominal GDP). China, interestingly, is taking another approach, throwing equivalent trillions into their real economy to make things as opposed to support paper, if only because exports are at the heart of their economic growth and they haven’t caught the American virus or suffered, I suppose, a “paper cut.”

At the center of U.S. policy support, however, rests the “extraordinarily low” or 0% policy rate. How long the Fed remains there is dependent on the pace of the recovery of nominal GDP as well as the mix of that nominal rate between real growth and inflation. My sense is that nominal GDP must show realistic signs of stabilizing near 4% before the Fed would be willing to risk raising rates. The current embedded cost of U.S. debt markets is close to 6% and nominal GDP must grow within reach of that level if policymakers are to avoid continuing debt deflation in corporate and household balance sheets. While the U.S. economy will likely approach 4% nominal growth in 2009’s second half, the ability to sustain those levels once inventory rebalancing and fiscal pump-priming effects wear off is debatable. The Fed will likely require 12–18 months of 4%+ nominal growth before abandoning the 0% benchmark.

Here is another way to analyze it. It seems commonsensical that because of asset market value losses over the past 18 months, the Fed must keep future real and nominal interest rates extremely low. Because

401(k)s have migrated to 201(k)s, and now 301(k)s, the negative wealth effect must be stabilized in order to reintegrate the private sector into the current economy. Renormalizing risk spreads – stock, investment grade, and high yield bonds among them – is another way to describe this hoped for foundation for future growth. PIMCO estimates that this process is perhaps 80–85% complete, which provides the potential for a sunny-side, right-side of the grass outcome, although still with New Normal implications. Still, investors must admit that without the policy guarantees of the Fed, Treasury, and FDIC, as well as the continuation of punitive 0% short-term rates that force investors to buy something, anything, with their cash, that risk spreads may widen again, not stabilize.

This somewhat detailed analysis on Fed funds policy rates should return us to my beginning thesis as to why they need to stay low: Asset appreciation in U.S. and other G-7 economies has been artificially elevated for years. In order to prevent prices sinking even lower than recent downtrends averaging 30% for stocks, homes, commercial real estate, and certain high yield bonds, central banks must keep policy rates historically low for an extended period of time. If policy rates are artificially low then bond investors should recognize that artificial buyers of notes and bonds (quantitative easing programs and Chinese currency fixing) have compressed almost all interest rates. But while this may support asset prices – including Treasury paper across the front end and belly of the curve, at the same time it provides little reward in terms of future income. Investors, of course, notice this inevitable conclusion by referencing Treasury Bills at .15%, two-year Notes at less than 1%, and 10-year maturities at a paltry 3.40%. Absent deflationary momentum, this is all a Treasury investor can expect. What you see in the bond market is often what you get. Broadening the concept to the U.S. bond market as a whole (mortgages + investment grade corporates), the total bond market yields only 3.5%. To get more than that, high yield, distressed mortgages, and stocks beckon the investor increasingly beguiled by hopes of a V-shaped recovery and “old normal” market standards. Not likely, and the risks outweigh the rewards at this point. Investors must recognize that if assets appreciate with nominal GDP, a 4–5% return is about all they can expect even with abnormally low policy rates. Rage, rage, against this conclusion if you wish, but the six-month rally in risk assets – while still continuously supported by Fed and Treasury policymakers – is likely at its pinnacle. Out, out, brief candle.

William H. Gross

Managing Director

About PIMCO

“PIMCO’s Mission is to Preserve and Enrich Client Assets and Provide the Highest Quality Investment Management Service.”

Who We Are

We are PIMCO, a leading global investment management firm with more than 1,200 employees in offices in Newport Beach, New York, Amsterdam, Singapore, Tokyo, London, Sydney, Munich, Toronto and Hong Kong.

We manage investments for an array of clients, including retirement and other assets that reach more than 8 million people in the U.S. and millions more around the world. Our clients include state, municipal and union pension and retirement plans whose beneficiaries come from all walks of life, from educators to healthcare workers to public safety employees. We are also advisors and asset managers to central banks, corporations, universities, foundations and endowments.

We are dedicated to our clients. From our founding in 1971, PIMCO’s global team of investment professionals has been dedicated to client service, allowing our portfolio managers to focus on returns. We serve individual investors through pooled and mutual funds in the U.S. and Europe and offer institutional clients mutual funds as well as privately managed separate accounts

We are committed to being the best provider of global investment solutions in the world. Our thought leadership, talent, technology and long-term investment approach drive our abilities around the globe. We offer a continually evolving set of solutions across all asset classes in an effort to provide investors with consistent returns, superior risk management and topflight client service.

We are a trendsetter in the asset management industry, and have been throughout our 38-year history. We remain at the forefront today, pioneering the use of innovative solutions for our clients, including portable alpha and absolute return strategies. Our investment process and operational structure drive our ability to anticipate client needs and respond quickly to ever-changing economic, market and policy environments.