For the better part of 40 years, the gold price has been standing guard over monetary policy. The gold price has been alerting investors to the potential threat of inflation. And if the recent price action in the gold market is to be trusted, this sentry has not fallen asleep on his watch. During the last few weeks, gold has jumped about 10% to over $1,000 an ounce.

But our story really begins in the late 1960s, just as “Lost in Space” was going off the air and the U.S. dollar was going off the gold standard. Back when B-9 was waving its arms and yelling “Warning! Warning!” once per week, the gold price was fixed at $32 an ounce and foreign central banks could freely convert their accumulated dollar bills for gold.

The French thought this was pretty sweet deal and swapped as many dollars as they could find for gold. However, President Nixon soon realized that this trade was a very sour deal for the U.S. And so, in August of 1971, he ended gold convertibility for good. Without this inconvenient and inhibiting link to gold, the U.S. discovered the pleasures of reckless monetary policy: printing dollars to pay debts.

Inflation kicked up almost immediately, as did the gold price. Within a few short years of ending gold convertibility, inflation jumped to double digit rates and the gold price jumped to $800 an ounce. But then the “yellow dog” took a good long nap. It slept through most of the 1980s and 1990s, as monetary inflation remained RELATIVELY tame.

By the late 1990s, the gold price had slumped to nearly $250 an ounce. It has been climbing steadily ever since. The initial move from $250 to $450 between 2000 and 2004 did not exactly scream “Warning! Warning!” But the gold rallies of recent years have taken on a more ominous tone, from a monetary standpoint. In other words, gold is in a bull market because inflation is in a bull market.

The most recent rally in gold seems particularly intriguing – and ominous – in light of the crazy quantities of cash that the Treasury and Federal Reserve have been tossing at the financial crisis. In various ways through various channels, the nation’s monetary bodies have conjured trillions of dollars into existence that did not exist before Lehman Bros. went bankrupt.

In all earlier epochs, such activities would have produced a large and inevitable inflationary trend. We predict this epoch will be no different. The gold price is telling us as much. So are the Chinese, as Byron King, editor of Outstanding Investments observed in a recent missive to his subscribers:

The Chinese Keep Buying Gold

“Then again, why worry about the future of energy development? The West — the U.S. in particular — is working overtime to wreck the future by debasing its currency and choking its economy.

“Don’t take my word for it. In a recent article, the U.K. Telegraph quoted at length Cheng Siwei, former vice chairman of the Standing Committee of the Chinese Communist Party. He explained how Beijing is dismayed by the ‘credit easing’ coming out of the Federal Reserve.

“‘If they [the Fed] keep printing money to buy bonds,’ said Mr. Cheng, ‘it will lead to inflation, and after a year or two, the dollar will fall hard. Most of our [Chinese] foreign reserves are in U.S. bonds and this is very difficult to change, so we will diversify incremental reserves into euros, yen and other currencies.’ Mr. Cheng was referring to over $2 trillion of Chinese foreign reserves, the world’s largest holding.

“‘Gold is definitely an alternative,’ said Mr. Cheng, ‘but when we buy, the price goes up. We have to do it carefully so as not to stimulate the markets.’

“Thus, we have direct testimony from a high-level cadre that China, while cautious, is a key driving force in the gold market. It’s buying. The implication is that the Chinese will not overbuy gold, which may be why the yellow metal has hovered just below the $1,000 mark per ounce in recent weeks. At the same time, it’s more than likely that China will buy gold whenever there’s a price dip.

“The significance is that the Chinese seem to be prepared to establish a floor under any correction in gold prices. This limits the downside for well-positioned gold miners such as AngloGold Ashanti (AU: NYSE) and Kinross (KGC: NYSE).

“As for the upside to gold prices? That will depend on when monetary-driven inflation begins to bite into the economy. The tide of inflation will lift the boats of the gold miners.

“Mr. Cheng’s greatest concern with the U.S. is that the country ‘spends tomorrow’s money today.’ Meanwhile, he added, ‘We Chinese spend today’s money tomorrow.’

“To sum things up, according to Mr. Cheng, ‘He who goes borrowing, goes sorrowing.’ Mr. Cheng was, of course, quoting that famous Chinese philosopher Benjamin Franklin.”

The Short-Term Case for Gold

Byron’s analysis above highlights the compelling long-term reasons to allocate some capital to the gold market. On a related note, most gold mining companies are swearing off the practice of “selling forward” – i.e hedging – their production. In effect, therefore, the insiders are buying…and that’s usually a bullish sign. “The size of the [gold] industry’s hedge book is set to drop to a residual of less than 200 tonnes by the end of 2010, the lowest in almost 25 years,” the Financial Times reported recently. “The reduction is a 95 per cent drop from 3,000 tonnes a decade ago.” The mining industry’s bullish stance is just one more vote of confidence in gold’s long-term investment appeal.

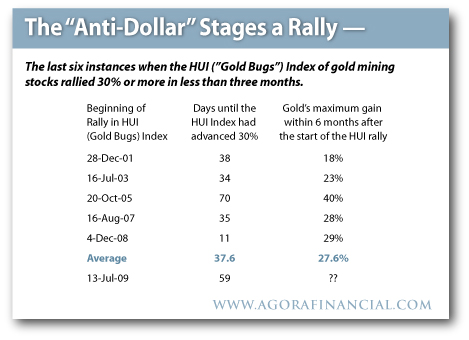

Meanwhile, the shares of gold mining companies are flashing a compelling short-term buy signal. Since late July, the gold mining stocks, as represented by the HUI “Gold Bugs” Index have jumped more than 30%, while the gold price has advanced only about one third as much.

As the nearby table illustrates, rapid 30% rallies in the HUI tend to bode very well for the gold price. The five prior instances in which the HUI rallied more than 30% in a very short timeframe, the gold price subsequently jumped an average of 27%. A similar advance this time around would land gold at $1,160 an ounce by Christmas – or about $140 higher than today’s price.

No such rally is certain, of course. But the monetary stars seem to be aligning for both a short-term and a long-term advance in the gold market.

Joel’s Note: With so much tumult in the markets right now, it can be difficult knowing exactly how and, perhaps more importantly, when, to buy gold. Has China created an impenetrable floor? Or will the September rally swoon, giving you a better opportunity a few weeks or months from now? Or, will the gold bull have already bolted by then? There’s plenty to doubt…

Eric J. Fry, has been a specialist in international equities since the early 1980s. He was a professional portfolio manager for more than 10 years, specializing in international investment strategies and short-selling. Mr. Fry launched the sometimes abrasive, mostly entertaining and always insightful Rude Awakening. His views and investment insights have appeared in numerous publications including Time, Barron’s, Wall Street Journal, International Herald Tribune, Business Week, USA Today, Los Angeles Times, San Francisco Chronicle and Money. He appears regularly on business news stations including CNBC and Fox.