The Rodney Dangerfield of All Investments

I awoke this morning to find an email from one of the financial journalists I really like and respect. It’s subject was “Gold’s Struggle.” Here’s an excerpt from that email:

“…I’ve noticed that despite most analyst expectations that gold will soon top, and maybe even topple over, the $1,000 mark, it has yet to do this with any conviction. The last time it climbed to a record high, many analysts were saying the price would climb so much higher — even to $2,000 in as little as 2 years. What’s happened to gold, why is it struggling to breach these price levels that so many were so sure it would breach and what would it take to make gold do what most people thought it would?…”

Despite outperforming most assets for quite some time (including the Holy Grail of investments, general equities), gold really never gets the respect it deserves. The reason for this is simple and must be understood by its buyers/lovers. 98% of all the players in the financial world are long financial assets. It’s not in their best interest to see gold going up sharply as it suggests all is not well within the “Don’t Worry, Be Happy’ crowd that greatly influences the financial services arena worldwide. In this case, gold is a thermometer and its taken the temperature of the world reserve currency and its owner and concluded the patient is terminally ill.

This journalist has been among the most open-minded towards gold I’ve known so you can only imagine what’s on the mind of most other journalists, many of whom make their living working with the “Don’t Worry, Be Happy” crowd every day. Don’t expect to find widespread support for gold in the media. It’s really the #1 go-to hate investment among all who apply their trade in and around the financial services industry.

Having said that, one journalist that has been favorable to gold’s appeal penned this column today.

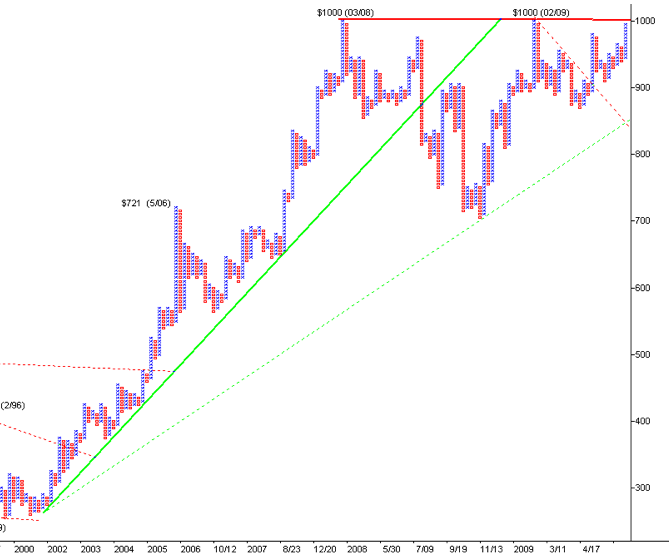

We remain in a secular gold bull market where it’s not a question of if, but when$1,000+ becomes a floor, not a ceiling. Don’t get caught up in gold’s ability or inability to get above $1,000 and stay there. Concentrate on the fact that it’s hovering at its all-time high and yet most of the world has missed the tremendous gains its afforded those of us for several years now. The party will be nearer its end when your neighbor stops speaking about how they’re trading Intel or Google but rather a mining stock they can’t even pronounced. This scenario isn’t even on the drawing board so party on dude!

Ed Note: click HERE for a larger, more easily readable version of the chart below. The larger chart also shows the action from 1982-2009. The snap below is just a section from 1999 – 2009 :

Some bullish articles for gold

This IMHO was dramatic news that the overall market yawn at but was extremely bullish for gold and very bearish for U.S Dollar

China is now a net seller of U.S. Treasuries

The following posted Sunday Sept. 6th/2009

Please note – I’m on a working vacation the next two weeks. My postings may not be as frequent as usual but I’m still here.

While all eyes were on the monthly employment statistics on Friday and what they may be saying about our so-called economic recovery, long-term investors should find this news far more concerning. What does it say about our country’s inability to increase employment over a ten-year period? While the financial crisis of the last 24 months has made many Americans wake up and take notice, they remain mostly unaware of the many other negative factors that were festering for years and the extent of how dire things were becoming.

U.S. Stock Market – The bullish argument may have taken a hit of late but it would be unwise to conclude the highs of this bear market rally are in just yet. Make no mistake about it, my stint in the bullish camp is over. However, it’s going to be tough to take the market down substantially from here while economic recovery remains evident in key parts of the world. The “Don’t Worry, Be Happy” crowd may be able to keep those “green shoots” tangling in front of their troops long enough to allow for a 10,000+ number on the DJIA. Again, I want no part of such a “final run” and am extremely comfortable sitting on spectacular returns afforded us these last 24 months. The fact that we continue to profit handsomely from the metals side of things only makes my sideline view easier. If we do get to 10,000 – 10,500, fantastic as it appears it would afford us the best selling opportunity since October 2007. It’s okay too if we just work lower from here because one would have a pile of cash to shop with again at the lower range of what I think is going to be a U.S. stock market range bound for years to come.

U.S. Dollar – A deeply oversold condition was noted several weeks ago and a window of opportunity for the dollar to rally was presented. So far poor Uncle Sam has merely managed not to go much lower. We’re at one of those points in time where both the cup half-full and the cup half-empty viewers can each make a decent argument. Such a time frame warrants careful attention as a significant move is near, only the direction is not identifiable as of yet. Therefore, I believe we would be best served to await one of two points to be taken out on a closing basis.

A close above 82 on the U.S. Dollar index would suggest a significant bear market rally was beginning while a close below 77 would suggest a test of the lows around 70 were now in the cards. Stay tuned.

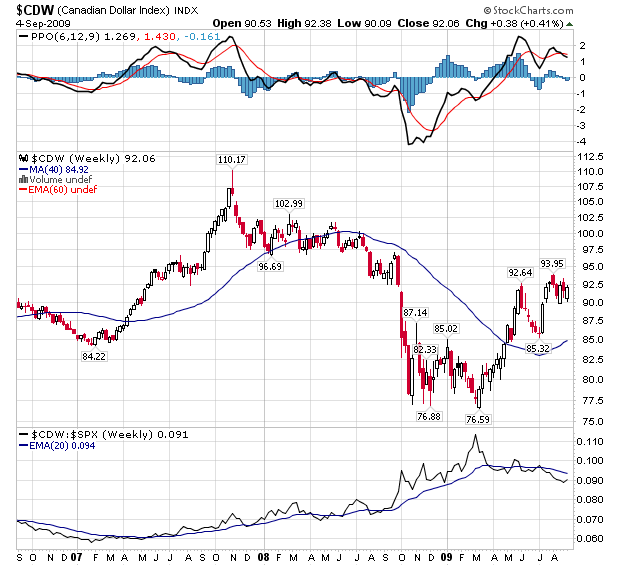

Canadian Dollar: I would like to note that I said the Canadian Dollar was my favorite currency back when it was trading well under 80 versus the U.S. Dollar. I went so far as to strongly suggest one should take savings in U.S. banks and convert them into Canadian dollars and place them in a Canadian savings institution. I did so on the belief Canada was in far better economic shape than the U.S. and the currencies would reach parity. I think both outlooks are proving to be correct.

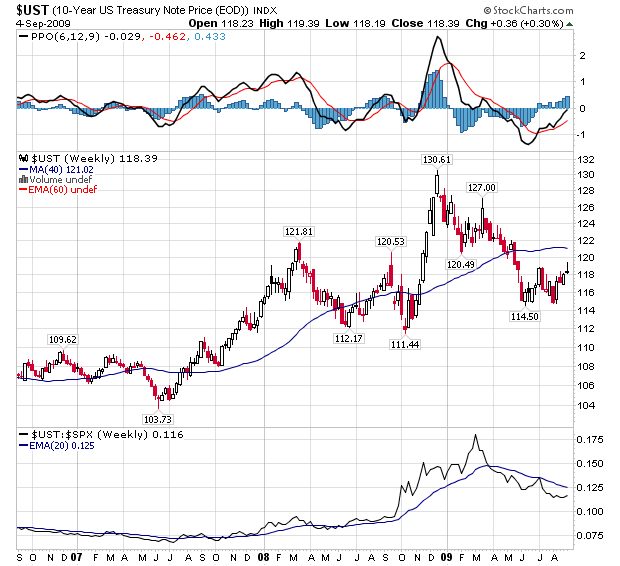

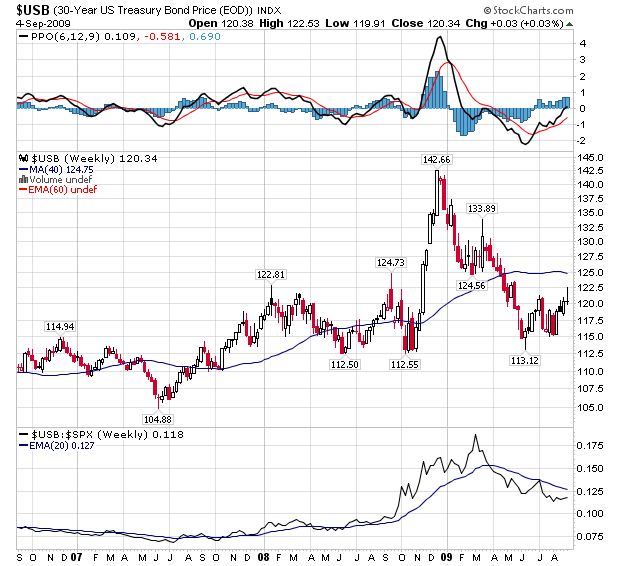

U.S. 10 to 30 Year Treasuries – Those of you scratching your head wondering how economic recovery can be underway yet interest rates are not rising, need to know you’re not alone. Well actually I do know and while its a bit frustrating at the moment, it’s only making the price to pay down the road that much bigger.

This was a very interesting piece of news that I believe you better put in the memory bank. I believe it’s yet another indicator of the days of China being a big buyer of Treasuries are behind us.

Oil – I continue to look for a $5-something price ($50-$59.99) before any new consideration of going long again.

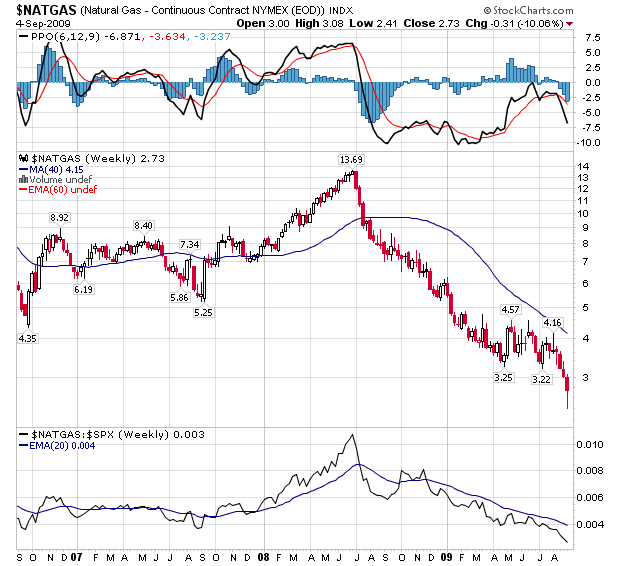

Natural Gas – While I’m no longer a growling bear on natural gas, I’m not quite yet to join whats ever left of the bullish camp (there has been widespread bullishness from several dollars higher, especially within the Canadian financial community and they have to be badly beaten up by now). I don’t think you’ve to be an “Einstein-type” to believe we’re going to see a cycle low between now and years-end. The question is do we try and time it to the day and hour or take a stab somewhere here knowing it could print down to zero before coming back to and above where we enter?

The addition question mark regarding natural gas is exactly how to play the long side? Because the oil and general equity market was strong, natural gas stocks were swept up in price. This has caused many to be overpriced. Do you step in when you think the gas price has hit bottom on the belief the shares will rise with a rebounding price and/or a continuing rising equity markets? Or do you wait because even if the gas price bottoms, the shares could come off because the fundamentals start to become reality in the share price and/or general equities go lower?

Stay tuned.

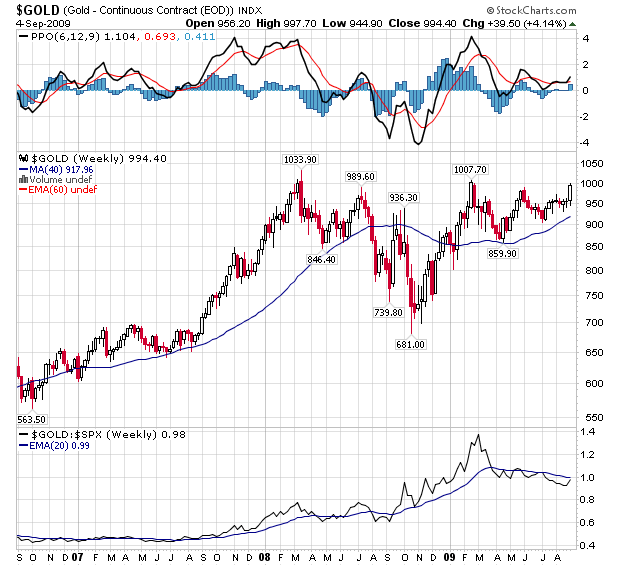

Precious Metals – Pardon me but I must point out how silly it is to me how certain commentators who continue to be far more wrong than right continue to be sought out for their opinions on gold. In the case of gold there are two who come to mind. Both have been horribly wrong on gold for years. I called them the “Andy Smith’s” of the 21st century (hard-core gold bugs understand this). While simply betting against them is not encouraged, it does personally comfort me when I’m on opposite sides of them.

I would welcome some consolidation and correction in the gold price in the coming days solely so it can go back to its normal place among the media – the back burner. Please know that this latest gold rally has not only been missed by many, it’s also being heavily shorted into. Both groups have been trying to talk gold back down. While they may have some very short-term success, the barn door is already open and a regular four-digit gold price to come is not a question of if, but when.

This is an extremely important bullish piece of information. And this doesn’t hurt either.

Model Portfolio Comment – The 5 stocks recommended just last Monday are up and average 20% in one week. I would look to buy any of them if we’re fortunate enough to get a pullback this week. If they just keep going straight up from here, we’ll have to just cry all the way to the bank. The portfolio has been updated.

Grandich Client Companies – With the summer doldrums behind us, I’ve begun speaking in-depth with company clients in hopes of bringing to you up to date information in the coming days and weeks.

On Major Moves, Grandich has been very right and not only saved many investors fortunes, but expanded them dramatically. On November 3, 2007 at the MoneyTalks Survival Conference, Peter Grandich of the Grandich Letter warned that “an unprecedented economic tsunami will hit American beginning in 2008”. Peter advised publicly to short the US market two days from the top in October, 2007 and stayed short until the last week of October, 2008. He began to buy stocks in March 7th, 2009. He also bought oil and oil related investments near the lows after the dive from $147.

….go to visit Peter’s Website.