Intermediate and junior oil service stocks have been pummelled by as much as 50% or more in three short months—even as all fundamental data showed a booming sector—both now and into Q4.

Canadian analysts say the market is either discounting a much larger correction in activity for 2012 or this is a great buying opportunity for investors.

National Bank summed up what the analyst group think with these two paragraphs:

“If hydrocarbon prices rebound to 2011’s average levels, the fundamentals for service companies will remain intact and 2012’s activity levels will likely be record-setting; therefore, these prices may currently represent a once-in-a-decade entry opportunity.

On the other hand, if the market is correct, service companies’ 2012 EBITDA will be approximately 25%-50% lower than analysts’ current estimates, and this would represent the second biggest pullback ever since 2009’s 38% decline.”

Rig counts in both Canada and the US are peaking at 4-5 year highs, and haven’t fallen yet. The number of wells being drilled in Canada in Q3 soared higher than anyone expected, trying to make up for a very wet Q2 that prevented thousands of wells from being drilled. Wells drilled in August and September were the most since 2006.

The number of operating days jumped 39% in Q3 over Q2, due to more intensive horizontal drilling, which is now over 60% of all wells drilled. As a result, service rig activity is high and rising. Deep horizontal drilling rigs are basically at maximum capacity now, which the industry normally doesn’t see until winter.

So while the business was on fire in Q3, the stocks were getting doused with water. That’s what has analysts – and investors – befuddled.

Valuations were lowered so hard and fast that four Canadian firms issued reports early last week saying the sell-off in service stocks was overdone, and valuations had improved enough to where they thought investors should be buying—at least a bit.

And investors were listening. Canadian fracking stocks were up 15% or more in the shortened (Canadian) Thanksgiving week, on great volume.

Said RBC Dominion, Canada’s largest brokerage firm:

“Our coverage universe on average is now discounting 2012 results that are ~18% below our current estimates, based on a return to historical trough valuation multiples.”

“While activity levels for 2012 will become clearer once E&P budgets begin to be announced, starting with Q3/11 results, we view the discount for certain companies as particularly pessimistic in the current oil price environment.”

Of course, the market isn’t discounting the current oil price environment—it’s discounting much lower oil prices, like the $65-$70 oil that oil producers’ stocks were pricing in last week and corresponding major drop in capital spending that goes along with that.

I attended an oil and gas conference recently in which one of the presenting CEOs was asked—at what oil price do you cut spending? He really did not want to answer, but it finally came out–$80/barrel. So that’s why this current price level is important to hold for services companies.

The four analyst reports I read suggested stocks were now pricing in a reduction in 2012 activity that ranged from 18%-30%–which usually means a 35%-50% decline in share prices. That is already priced into the services stocks and then some, creating this buying opportunity, they say. (FYI, frackers have more leverage to producers’ spending levels than drillers, which gives their stocks bigger swings; they’re more volatile stocks.)

Analysts outlined several factors that they think could make this downturn in the oil services cycle different than before.

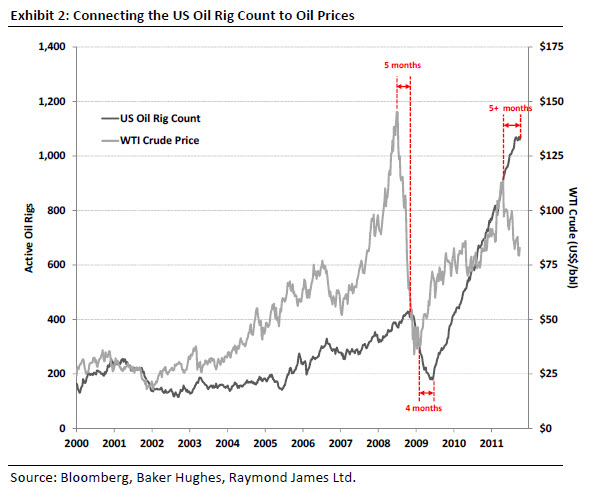

One factor is…well…it has been different before. Raymond James, a brokerage firm on both sides of the 49th parallel, says that between June 2009 and September 2010, the oil services stocks lost 38% of their share value—while the rig count kept going steadily higher, without even pausing.

That is the only time the market priced in a downturn in activity, and it didn’t happen. Raymond James pointed out that the rig count in both Canada and the US has now plateaued, “almost as if it’s trying to decide if the hitherto sound fundamentals or the forward-looking bearish technicals will win the day.”

The US onshore rig count stopped going up in August, and the Canada followed suit in mid-September. But they haven’t fallen, and Raymond James says it’s highly unusual for oil to go down 5 months like it has and not see a corresponding drop in rig count. It’s definitely a chin-rubber.

Another point is that for the first time ever, North American rigs are drilling mostly for oil, not gas. Previous cycles have all been predicated on the continental natural gas cycle—which is generally more volatile than the global oil market. Really. 😉

Even the natural gas rig count in the US is up for the year right now, despite very low prices and a bearish outlook.

Why? I would suggest it’s because gas rigs are now drilling for Natural Gas Liquids (NGLs) like ethane, propane, butane and condensate—and they can afford to sell the regular, dry natural gas at a low price. NGLs receive world pricing, and a lot of US produced NGLs end up in Latin America now.

The point is that the underlying commodity cycle for the services sector is different in North America now.

Toronto-based Cormark Securities mentioned several other items in their report:

- More long term contracts for drillers and frackers (or “pressure pumpers”)—the drilling fleet is 25% under contract, while pressure pumpers are enjoying >60% of capacity contracted in the US and ~50% in Canada

- Large joint ventures with National Oil Companies (NOCs) and other International Oil Companies (IOCs) have given US & Cdn E&P companies $21 billion to spend since early 2010 (they listed 21 different deals)

- Land sales. The industry has spent $3.4 billion on new land leases, with most of it in areas that already have excellent infrastructure, meaning access is easy to get in and the oil/gas is easy to get out (I would add that for Canada, if the newly tested Duvernay formation gets deemed commercial in Q1 2012, the entire services sector in the Great White North will continue to laugh all the way to the bank.)

Will this downturn cycle really be different for Canadian and US service companies? It has happened once before. Or are energy stocks – both the producers and the service companies – foretelling of lower oil prices and reduced spending in 2012?

RBC says investors should stick with the deep drillers; the trend is to deeper, longer horizontal wells. Cormark says go with the defensive large cap names with good liquidity. National Bank says go with geographic diversification and technological sophistication.

No matter the choice, investors will need to be nimble in this market.

– Keith Schaefer

Publisher, the Oil & Gas Investments Bulletin

To contact Keith on editorial issues, email him at: editor @ oilandgas-investments (dot com). Due to volume of email, Keith cannot guaranteed that he can answer each question individually.

For answers to common problems, such as changing your password or logging on, please refer to our Frequently Asked Questions page.

For all other issues, such as if you are a subscribed member and are having problems logging in or billing, please send an email to customerservice@oilandgas-investments.com beforephoning the customer support line.

The customer service email address is monitored 7 days a week while the phone line is only monitored during business hours, Monday to Friday.

Customer Service phone number: 1-877-844-8606