Ed Note: Conclusions moved from the bottom of this article to the top.

Conclusions

While risk assets remain overbought (see stocks and commodities sections above) and the USD appears well oversold, we await a catalyst to start the countermove. For the USD, the best prospects are an overall pullback in stocks, and possible central bank intervention.

Other Conclusions

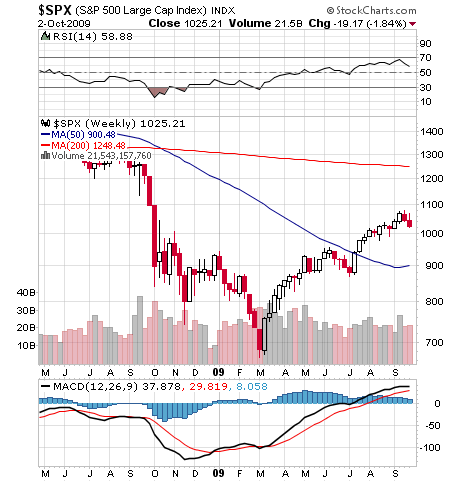

With no real resistance on the S&P 500 before another 5%, momentum from profit taking alone could carry it down to around 980, with other risk assets likely to follow. There’s little influential news on the calendar for the coming week, so the likely bias is to tight range-bound trading with a bias down a few percentage points.

The overall theme this past week was a distinct reversal in risk appetite, as global equities, commodities, and related risk currencies pulled back while safe haven assets gained. A disappointing US employment report justified the pullback, though minor losses suggest it was mostly priced in already.

STOCKS

Because global currency and commodity markets follow global stocks, which in turn tend to follow the S&P 500, we open with a quick look at it. Key points:

Closed lower for the second straight week as markets correctly anticipated disappointing jobs results.

A light news week ahead suggests no huge moves until Q3 earnings, unless sentiment has already turned negative enough for equities to continue to pullback on profit taking.

Will “bad results beating even worse expectations” allow stocks to rise again as they did in Q2, despite their further gains since then? Common sense says no, but it said the same thing last time.

Recovery sentiment & news over past months was heavily dependent on temporary stimulus and inventory restocking. As such, further gains will depend on genuine self sustaining recovery in fundamentals, but we don’t see that yet. Instead, much of the news is of the “slowing decline” theme.

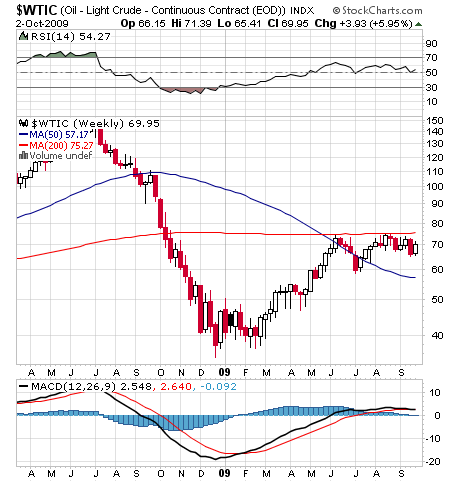

COMMODITIES

They continue to follow equities, though not necessarily day by day or by the same magnitude. For the most popularly watched commodities like crude oil and gold, speculators, including the small, least informed ones, remain overwhelmingly long, and the reputedly more reliable commercial traders tend to be short. That suggests more risk to the downside, as does the past week’s moves in stocks combined with their already extended rally.

CURRENCIES

USD

US Dollar Recovery Depends on Continued Stock Pull Back, Central Banks Might Help

Summary

Fundamental Outlook for US Dollar: Bullish

Friday’s NFP disappointment will likely dampen risk appetite and help the USD, which mostly moves in the opposite direction of stocks.

USD may have set an important bottom against the Euro.

US Unemployment Rate hits 26-year high on NFP disappointment.

US ISM Non-Manufacturing, 80% of US GDP, is a key barometer on domestic economic activity and the main US news for this week.

Analysis

The US Dollar finished the week higher against the Euro and other key counterparts, but a sharply disappointing Nonfarm Payrolls report nearly derailed the nascent USD recovery through Friday’s close. The trade-weighted US Dollar Index hit fresh monthly highs near 77.50 just ahead of the release.

Immediate declines in the US S&P 500 initially sent the dollar higher, but markets clearly expressed their displeasure with the worse-than-expected payrolls release and sold USD through in subsequent trading on poorer US fundamentals. The risk aversion the NFP created is likely to provide a longer lasting boost for the USD, which trades up mostly on risk aversion and is heavily shorted already.

US CFTC Commitment of Traders data shows that Non-Commercial traders—a group mostly comprised of hedge funds and other large speculators—remained the most net-long the Euro/US Dollar since it traded near 1.6000 in early 2008.

The sentiment generated by the coming Q3 earnings season is the likely catalyst for the next big move in risk sentiment and the USD.

Events

US Dollar traders should be alert for abrupt shifts in risk sentiment, but a relatively light US economic calendar leaves limited chance for major daily volatility. The notable exception is Monday’s US ISM Non-Manufacturing report, which will shed further light on the state of the domestic services industry. According to 2008 estimates, the Services industry accounts for nearly 80 percent of US GDP. Suffice it to say, any noteworthy surprises in the highly-anticipated report could force major moves in the US Dollar and broader financial markets. Indeed, the ISM Non-Manufacturing survey tends to be one of the most market-moving events on release. Pay particular attention to its employment component, which could worsen or soften the impact of Friday’s NFP let down.

Outside of the ISM report, forex traders should keep a look out for a number of important global central bank interest rate decisions. Uncertainty surrounding Australian, British, and European central bank announcements may create some movements across key forex pairs. However, these tend to be unpredictable, so traders must focus on cutting risk on trades in the hours before and after these announcements.

While there are early signs of a sustained US Dollar reversal, recent price action has shown markets were not yet willing to push the Greenback materially higher versus key counterparts. The coming week may prove especially important to overall trends in major US Dollar pairs. Traders should watch the S&P carefully for signs of how risk and safety currencies could behave.

EUR

Its Fate Depends on Risk Appetite, ECB Might Help

Summary

Fundamental Forecast for Euro: Neutral

EU receives the results of its own financial stress test: the prognosis is promising, but is it credible?

Euro Zone Unemployment is now at a 10-year high of 9.6%.

German and regional inflation gauges still pitched into negative territory.

Moving with overall risk sentiment as shown by the S&P 500 pullback, thus falling against the USD, gaining against riskier forex like the AUD.

Euro-zone growth projected below that of US and Japan, along with ECB pro-USD comments, making EUR more vulnerable.

Analysis

Just this past week, the EU completed a five-month long stress test of its financial markets. In the end, none of those institutions surveyed were expected to see their tier one capital ratios fall below 6 percent (the Basel minimum is 4 percent) even in the worst of conditions. However, skepticism is likely to develop just as surely as it did after the US test. It is reasonable to question why there were only 22 banks for such a broad region and with what methodology they measure risk; but the real concern is in the 400 billion euros of additional losses the market could sustain under the most extreme conditions. We have already seen 489 billion in losses so far. The IMF suggests European banks have disclosed only 40 percent of their losses.

Maintaining the pace of production after inventories build up and facilitating consumer spending will be the keys to sustainable growth. Recently, Trichet stated that a healthy dollar was “extremely important.” This can be interpreted to mean he is very concerned about the high level of his own currency, and that bodes badly for the EUR/USD.

Events

Monday brings Euro-zone Sentix Investor Confidence, and Retail Sales m/m, Wednesday EZ GDP q/q and Geman factory orders, and Thursday brings an ECB rate announcement and German trade balance. With the central bank already announcing it was culling its unlimited fund auctions, we already have the first steps towards hikes, so we will have to absorb everything said after this week’s rate decision.

JPY

Testing Major Resistance, Movement Follows Overall Risk Sentiment

Summary

Fundamental Forecast for Japanese Yen: Bullish

Japan’s Jobless Rate Unexpectedly Falls, Household Spending Surges.

Business Outlook Improves But Capital Investment Falls Most in 10 Years.

Housing Starts Fall Most in Two Years, Industrial Production as Expected.

The Japanese Yen will begin the week ahead at a crossroads, with the behavior of risk appetite likely to set the direction. Global equity markets slumped for the second consecutive week amid increasingly mixed economic data capped by September’s disappointing US jobs report. If we are indeed at the brink of another downturn for equities, as suggested in the above stocks section, the spectrum of risk-correlated investments (commodities, carry trades) are very likely to follow, with the Japanese unit rising as traders unwind short-Yen yield-seeking positions, threatening to send USD/JPY below the 80.00 mark for the first time since 1995.

Events

The economic calendar is fairly tame compared to last week’s overload of significant releases, and much is already priced in, making these unlikely to move markets.

GBP

Data and BoE Pressuring the Pound

Summary

Fundamental Forecast for British Pound: Bearish

Last week’s reversal looks more like a temporary relief bounce, occurs without underlying economic improvement

UK GDP was revised to -0.6% in Q2 from -0.7%, annual rate at record low of -5.5%.

Mortgage approvals in the UK eased down to 52,300 in August, indicating lingering pressures in the housing market.

However, Nationwide Building Society said UK house prices rose for the fifth straight month in September.

Analysis

While a handful of fundamental reports from the nation have been slightly better than expected, such as the 0.9 percent rise in Nationwide house prices, more often than not, they are countered by contradicting data, such as the drop in the purchasing managers’ index (PMI) for the construction sector to 46.7 in September from 47.7.

Events

The services sector is improving. PMI for the UK’s services sector has consistently held above 50 since May, indicating an expansion in activity, and data due to be released on Monday is likely to show a continuation of the trend in September as PMI is projected to rise to a two-year high of 54.5 from 54.1. However, with the unemployment rate in the UK also steadily rising, there are some downside risks for the sector, and consumption as a whole.

The main event risk for the British pound will be Thursday’s BoE rate decision. It’s the BOE’s accompanying policy statement, not the rate announcement itself, which has consistently been the prime “news event” of recent rate decisions. If it suggests no additional stimulus that should support the GBP, and the opposite would do the opposite.

CHF

Support Likely Despite SNB Intervention Threat

Summary

Fundamental Forecast for Swiss Franc: Bearish

The KOF leading index for September rose to 0.85, its highest level in a year.

UBS Consumption Indicator Fell to 0.658 from 0.747, the lowest since December 2003.

The SVME- PMI Jumped to 54.3 from 50.2, the highest in 15 months.

SNB demonstrated again its willingness to keep CHF low against the EUR

Jobs and spending expected to remain depressed

Analysis

The USDCHF ended the week erasing gains from a mid-week spike that was rumored to be intervention from the Swiss National Bank. The synthetic price swing was much more evident in the EUR/CHF giving credibility to the theory. The central bank had no comment following the sudden Franc deprecation which wasn’t as obvious as the actions taken in June and March but may have been a mere reminder to markets that they stand ready to prevent further appreciation. On the week there were a number of significant fundamental indicators that gave a conflicting picture for growth.

Events

Risk sentiment continues to have influence on price action for the pair as the dollar has been strongly correlated with demand for high yielding assets. Traders should keep an eye on this week’s releases which include unemployment and consumer prices.

CAD

Tracking Crude Oil First, Stocks Second

Summary

Fundamental Forecast for Canadian Dollar: Neutral

Canadian Finance Minister Flaherty says currencies will be brought up at the G7 meeting.

Canadian Prime Minister Harper avoids a “non-confidence” vote to maintain power.

Continues to trade with oil, stock movements, suggesting more downside

Analysis

Fundamentals and sentiment have been long been out of alignment; and the patterns that we have seen develop in key currencies, equities, bond funds and other market areas may signal that we may find resolution soon, more likely to the downside as risk assets are still in an extended rally beyond apparent justification by fundamentals.

Events

Despite how the underlying current of risk appetite develops over the days and weeks ahead, we should also keep our eye on key economic data to cross the wires. This is important not only for short-term bursts of volatility but for the outlook for growth and interest rates as well as the currency’s ultimate standing in the risk spectrum.

There are more than a few significant economic releases due over the coming week; but topping the docket is Friday’s labor data. As with most economies, domestic consumption is vital to Canada. However, the jobs outlook isn’t bright. Given the considerable influence consumer spending will have, expect sensitivity to significant surprises in the jobs numbers. Exports could help, but most are to the equally stagnant US, rather than faster growing Asia.

AUD

Is the AUD Consolidating or Reversing? Likely to Continue to Follow Risk Sentiment as Represented by the S&P 500 Index

Summary

Fundamental Forecast for Australian Dollar: Bearish

Australian retail sales rose for the first time in 3 months during August.

The TD Securities’ inflation index fell to 1.3%, the lowest since records began 6+ years ago.

Unemployment data and rate decisions likely to show Australia in relatively good shape – but isn’t that already priced in?

Analysis

The Australian dollar was the weakest of the major currencies last week, and a bearish engulfing candle on the daily AUD/USD charts on October 1 suggests further declines could be in store. Since the Australian dollar still tends to move with other risky assets, traders should look for any fallout from the release of the G7 statement over the weekend regarding a coordinated intervention effort to boost the USD.

Events

Later in the week, the Australian dollar is going to encounter two of its most market-moving reports: a rate decision from the Reserve Bank of Australia and the net employment change.

On Wednesday, the net employment change for the nation is anticipated to fall, and the Australian unemployment rate is projected to edge up to a 6-year high of 6.0 percent, which still seems sunny when compared with other regions like the US, the UK, and the Euro-zone.

NZD

May Weaken as Growth Rate and Trade Falter, Vulnerable to Profit Taking

Summary

Fundamental Outlook for New Zealand Dollar: Bearish

New Zealand Business Confidence surges to decade high

New Zealand Dollar sentiment at clear bullish extremes – top is near

Analysis

The New Zealand Dollar finished the week almost squarely unchanged against its US namesake, as a noteworthy pullback in global risk sentiment offset several bullish NZD data releases. Yet we cannot deny that overall survey data points to a return to economic growth—however moderate—in the foreseeable future. Limited economic event risk in the week ahead means traders should instead keep a close eye on broader financial market risk appetite as seen through the US S&P 500.

The combination of the deterioration in global financial risk sentiment and overextended NZDUSD positioning leads us to believe that New Zealand Dollar risks remain to the downside. Whether or not the NZD turns lower will very much depend on the trajectory in the S&P 500 and broader risky asset classes.

Events

No major events.

Conclusions

While risk assets remain overbought (see stocks and commodities sections above) and the USD appears well oversold, we await a catalyst to start the countermove. For the USD, the best prospects are an overall pullback in stocks, and possible central bank intervention.

Conclusions for the Above Instruments

With no real resistance on the S&P 500 before another 5%, momentum from profit taking alone could carry it down to around 980, with other risk assets likely to follow. There’s little influential news on the calendar for the coming week, so the likely bias is to tight range-bound trading with a bias down a few percentage points.

For the best high dividend stocks: http://highdividendstocksguide.blogspot.com

Cliff Wachtel, CPA, is the Chief Analyst for AVAFX, a leading online trading site for global currency,commodity, and stock index trading, at www.avafx.com. He is also listed in the Who’s Who of Financial Bloggers. He has served as investor, writer, and advisor on stocks for many years. In addition to forex, commodities, and stock indexes, he writes on quality high dividend stocks — those with high, sustainable dividends backed by sound businesses with solid fundamentals. The goal is to provide high, reliable income through down markets and have better long term appreciation potential than bonds, and also better liquidity and lower, more transparent trading costs. Cliff is married with 5 children and too many pets to count.

To get fastest access to posts:

for Global Forex, Commodities & Stocks go to: http://worldmarketsguide.blogspot.com