This article from the Creative Education site Minyanville.com Get a Free Membership HERE (top right)

Hunting Down Predators for Big Returns

Christian Andreach isn’t betting on a strong rebound here in the US. But the 36-year-old professional stock picker is wagering on faster growth overseas, a view confirmed by the many C-suite executives he chats with every week.

“They see things getting a little better,” says Andreach, a managing director at Manning & Napier Advisors. “Things are stabilizing. That said, those same companies are looking abroad for the next leg of growth.”

Andreach agrees. So, along with six other managers and analysts that run Manning & Napier’s Equity Series fund (EXEYX), he has placed big bets on companies with large global footprints. The team uses a bottom-up approach that isn’t tied to one style: They look at growth, cyclical, and deep-value plays.

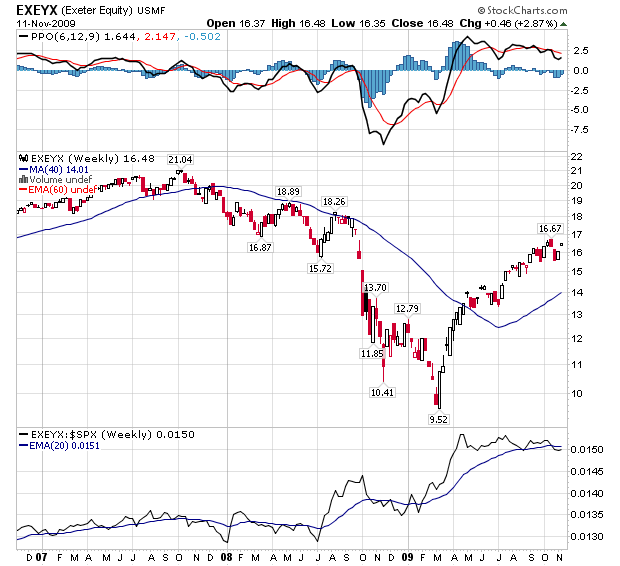

The strategy works. Morningstar fund analysts write that EXEYX has produced outsized returns in a variety of buoyant markets, and has also held up better than nearly all its rivals in bear markets.

Through November 9, the five-star fund’s 10-year annualized return of 5.95% leads the S&P 500 by 6.39 percentage points, and bests its Morningstar rivals by 8.12 percentage points, placing it in the top 1% of its category.

The no-load fund, with $1 billion in assets, has an expense ratio of 1.05%, and minimum investment of $2,000.

Recently, we caught up with Andreach at his office in Fairport, New York. We talked about his top picks right now, including Google (GOOG), Monsanto (MON), and General Mills (GIS), and why he’s steering clear of the banks.

Minyanville: Explain the fund’s investment strategy for us.

Christian Andreach: We have three strategies. First, there is the “profile strategy”: We look at companies that have strong market positions, good growth prospects, and are selling at reasonable prices. We look to buy a stock when it is trading at around 20% below fair value.

Minyanville: And the second strategy?

Andreach: We employ something we call the “hurdle rate strategy.” It’s our strategy for investing in cyclical industries. Whenever returns are very high in an industry, competition comes in and that drives returns down below the hurdle rate, the break-even rate of return on investment. We like to invest when industry returns are low and capacity is exiting the business and sell when industry returns are high and capacity is turning into the business.

Minyanville: The final strategy?

Andreach: It’s our “bankable deal strategy.” This is our deep-value strategy. We estimate a fair value of an enterprise and look to buy it at $0.50 on the dollar. Price becomes its own catalyst. At a certain level, market forces come in and realize the value in the enterprise.Minyanville: You also target companies that benefit from the pain of their competitors. Elaborate on that for us.

Andreach: We might not be able to bank on the macro outlook providing a strong tailwind to business, but we might have identified a troubled competitor losing market share. So we can invest in the company on the other side, which is gaining. In sum, we are looking to capitalize on the companies that are exploiting the weakness of others.

Andreach: Exactly. It’s also why we like Southwest Airlines (LUV). We see them as the low-cost operator in the industry. Demand is still a wild card. In response, supply is coming out of the airline industry. That supply is coming out from Southwest competitors. So, when demand comes back, Southwest will be in an advantaged position — they didn’t cut back on supply, and they have a low-cost position that will help them with price.

Minyanville: Your holdings carry much less debt than the typical large growth fund.

Andreach: It’s a bi-product of our investment strategies. When we invest in a company, we will penalize that company in terms of the price we’re willing to pay for it if they have what we see as excess leverage. As a firm, we are biased against credit risk.

Minyanville: How important is management to you?

Andreach: It is important. We want to make sure that we’re on the same page as management.

That being said, we are investing in a business. The quality of the business is more important than just the individuals running that business.

I’m not saying that management is irrelevant. It’s just that even the best management team will have a hard time creating shareholder value in a business that just isn’t a value generative business. Even the nicest, smartest guys in the room won’t push us into an investment that doesn’t fit what we do.

Minyanville: You beat 99% of your peers over the 10-year period. What does your team do differently than the competition?

Andreach: First, we have defined investment strategies.

Second, each strategy has a certain pricing discipline associated with it. It must fit our knitting and it must sell at a price that affords us an attractive rate of return going forward.

Third, when we buy a stock, we have set a fair value for that stock. We are specific about when we buy and sell. We just don’t let things run. We have a risk-managed approach that dictates when we get in and out of positions.

Minyanville: Let’s do some stock picking. What is your thesis on Google, the fund’s largest holding?

Andreach: We are going to reach a tipping point when those 18- to 24-year-olds in college and business schools will become brand managers. They will know that the consumers of tomorrow are online and are on their cell phones. You will see a fall in traditional media.

This will help players like Google. The company is active where the eyeballs are. Google is where we will see secular growth going forward. We are now in the middle of a major advertising recession, but you wouldn’t know that if you looked at Google’s numbers. They are taking gobs of share of a very large pie.

Minyanville: How about Monsanto? Looks to me like you have been adding to this one.

Andreach: Yes, this is a simple story. There are some near-term issues, but the fact is that the developing world is growing. There is an emerging middle class, which is demanding more protein. That means you have to raise more animals, which means you need more animal feed. So you need more corn and beans.

Minyanville: But there’s a relatively fixed stock of acreage.

Andreach: Right, so you need to increase the yield on each acre. Monsanto provides the tools necessary to improve yields.

Minyanville: The stock is down about 15% over the last six months.

Andreach: The stock price hasn’t been performing that great recently. Over the next year or so, bottom-line growth will be challenged. They have a Roundup business that has suffered from an influx of Chinese generic product, so they had to lower prices. But that will work itself out over the next year or so. Then the market will once again focus on the underlying growth in the drivers of the company’s profile going forward.

Minyanville: Turning to consumer staples, what’s to like about General Mills and Kellogg (K)?

Andreach: We bought these back in April. We are biased toward companies that have stable demand for their products. Both of these companies do. They sell at reasonable valuations, and they have very strong cost controls.

Also, if you believe in a return to some level of inflation, then you should focus on companies that show an ability to offset that inflation.

Minyanville: How do you feel about the banks?

Andreach: The truth is, we are still working through the process of getting the banks healthy. We are seeing elevated loan delinquencies. The yield curve is very steep right now. It’s tough to see how it will get much better for plain vanilla banks than it is now. And, of course, there is the commercial real-estate shoe that some feel has yet to fall. Banks are one area that we have a hard time getting comfortable with.

Minyanville: Thanks for your time, Christian.

Here are the categories on Minyanville.com:

BUSINESS & MARKETS LIFE & MONEY AUDIO & VIDEO FAMILY & FINANCE SUBSCRIPTIONS & PRODUCTS OPTIONSMITH BY STEVE SMITH BUZZ & BANTER JEFF COOPER’S DAILY MARKET REPORT FLEXFOLIO HOOFY & BOO 5 THINGS RANDOM THOUGHTS UMV MINYANLAND EMAIL ALERTS MV EXCHANGE ARCHIVES THE WEEK’S ARTICLES DICTIONARY PROFESSORS