Benefits of Cash-Flow Real Estate in General

How profitable is real estate? VERY!

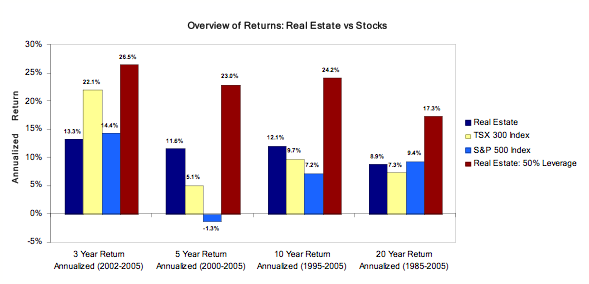

The following chart shows the overview of historical returns of stocks versus real estate. As you can see, un-leveraged real estate has outperformed the stock market for over 5 years and 50% leveraged real estate has outperformed the stock market over any period – including down markets.

The benefits of cash-flow rental real estate assets in your portfolio are very evident from the historical returns of such assets when compared to other capital gain assets such as stocks. Like stocks, real estate goes in cycles, and therefore you want to buy in an upswing or emerging market, in an area where people move to, where income is strong and rents are going up or at least, are steady. Many US states are such markets as of 2008, despite all the negative press about falling US house prices. When house prices fall, even more people chose to rent, benefitting you, the (future) landlord or co-owner of an apartment building.

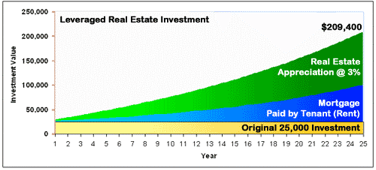

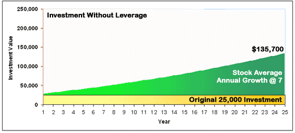

Here are some assumptions we made to calculate the yields in the following pages: Annual return for stocks is 7% and annual appreciation of real estate is 3%. If the rate of growth is less for real estate, why is a $25,000 investment worth more after 25 years?

Real Estate is a Leveraged Investment

While a bank would usually not put up 75% of the cost for an investment in stocks, bonds or mutual funds, a bank will provide 75% of the cost for an investment property, or even up to 85% if it is CMHC insured.

Banks do not like to take risks, hence they consider a leveraged stock investment to be risky.

This picture assumes a cash investment of $25,000 for a $100,000 property (for example a condo) and an annual appreciation of 3%. As you can see, in 25 years the property is worth over $200,000 and is still providing monthly income! You have increased your investment 8-fold. Even in the worst case scenario of flat real estate, you have an asset worth 4-fold, which you own 100% and which is still providing monthly income. Even if the real estate drops 50% in value (extremely unlikely) you have doubled your money.

Well-researched leveraged real estate investments, on the other hand, are not considered to be as risky because they are secured by real property – hence the name “real” estate – unlike stocks which often use factors like P/E ratios or projected future earnings to arrive at some share price. Remember ENRON ? They hid details about their debts in so called SPEs (Special Purpose Entity) to show higher profit. How about WorldCom ? Martha Stewart rings a bell ? Conrad Black and Hollinger International ? Go for “real” assets with real value where real people pay real dollars every month, in every economy.

The Benefits of a Leveraged Real Estate Investment

An investment in stocks, bonds or mutual funds will buy the equivalent amount of equities. In other words, $50,000 buys $50,000 of equities, unless you buy on margin. A leveraged real estate investment buys real estate worth many times the down payment. A property worth $100,000 can be purchased with $25,000 down payment – or less if it is CMHC insured. You benefit from growth of the property total value, not just the original investment, which multiplies your returns.

The principal of the mortgage is paid down by your tenant who – over time – essentially buys the investment for you.

Calculating Real Estate Returns

Unlike a stock where the only measurement of a return is the price increase of the equity (see chart above), there are 3 to 4 factors which contribute to the overall return in a real estate investment. They are:

- Property Appreciation (the green area) – often the largest return on a long term hold asset which is held with the intention of producing rental income like our LPs. This appreciation is tax free, until sold, like an RRSP, and then it is usually treated as capital gains which is taxed at only 50% of regular income – or it is taxed as a dividend if held in a corporation or in a US corporation as a non-US resident !

- Principal Reduction of Mortgage (the blue area) adds to the equity but is paid by the tenant in the form of rent.

- Positive cash flow could be negative to very positive or even substantial in Prestigious Properties investments – especially in the latter years ! Normally, you want to have positive cash flow from day one but often we re-invest all the cash flow into the building in the first 9 to 15 months after acquisition to improve the building, and thus the value one to three years down the road.

- Possibly, tax losses in year one or two of a venture. This figure is usually 0 in a joint venture, but could be a small amount in a limited partnership scenario (don’t invest in a venture where the key benefit is a tax loss! Always, always treat a possible tax loss as a bonus and don’t include in your calculations).

In a Real Estate Investment:

- Your tenant or tenants pay down the mortgage which increases your return and essentially buys the investment for you.

- Each time your mortgage is reduced, your investment return increases.

- There is usually an initially small, later larger amount of money remaining each month even after mortgage and other expenses are covered (note this is usually taxable as income !).

- This money also contributes to your overall return.

- Even though you’ve only put up a portion of the cost of the entire investment, you benefit from the entire growth of the property value.

Income Streams from Real Estate

Once the principal on your investment is paid, or even well before it is paid off in its entirety, the monthly rental payments from your tenant become monthly income for you.

- Rent generally doubles in Canada or US growth markets every 15 years (this is over 4% annually – more than the 3% real estate growth we have assumed earlier !).

- Rental income is a great way to hedge against inflation as it increases with inflation, and in most cases at a quicker pace – important in the future as US or Canadian interest rates and thus inflation may rise in the latter half of this decade

- Owning 5 or 6 properties, or a share in a Real Estate Limited Partnership, can generate a substantial monthly income that will continue to increase with your life expectancy.

- The property is managed for you – there are no property management hassles (this is a major reason why many people shy away from real estate investments)—we make it easy for you!

- The key is POSTITIVE CASH FLOW: more money comes in than flows out! This is not possible in many parts of the world because prices are so high that rental properties don’t make sense unless purchased with very large down payments such that ROI’s get smaller and smaller.

Calculating Stock Returns

Unlike real estate, the only measurement of return on most stocks is when its price goes up (see chart). To generate income from a stock or mutual fund, the investment must be sold, unless it is a dividend rich stock.

Real estate produces income each and every month while at the same time the mortgage is usually paid down while the value of the property usually increases – and it is inflation proof – and it is a good investment even if the economy is flat or declining – there is always a demand !

Where to buy .. and where not to

Like a farmer, we also have different seasons for investing. Obviously, a season is usually longer than a year – sometimes a decade or two.

1) Real Estate Winter – time to study the markets, do your research and wait for the buy signals.

2) Real Estate Spring – this is when the fundamentals start to look strong and prices are poised to increase. This is when we buy property.

3) Real Estate Summer – the fundamentals continue to look strong. This is when we hold and improve our properties.

4) Real Estate Fall – the fundamentals show the value growth is slowing down. This is the time to sell many properties and prepare other properties for winter.

Profit Potential: Enormous with prudent leverage !

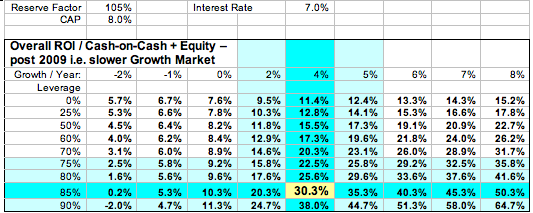

Over the last 6-7 years, Properties that have been acquired in Alberta or Saskatchewan with high leverage in areas of high growth have yielded great returns. As you can see in the chart below, with leverage of 85% and growth at 8-15% per year have been able to consistently provide cash-on-cash returns well above 40% to 60% PER YEAR. Neither AB nor SK apartment building values will not likely grow at 8-15% per year going forward, but still a respectable 4-6% and with property values much higher in AB or SK, we are now only able to purchase buildings with 50% to 60% leverage. Since we require more cash to close (less leverage), the ROI and cash-on-cash ROI will be lower than in previous years!

As shown in the chart below, even with higher interest rates, higher CAP rates and more moderated medium growth in select slower growth markets one can are deliver a higher cash-on-cash ROI investing in buildings with high leverage. Investing in these areas also provides us with better cash flow – an important element when holding longer term !!

Investment Approach – How to select properties for very high cash-on-cash returns

Locate under-managed, under-valued properties in growth areas of promising cities or emerging markets in North-America. With this mind, we use the following four steps to evaluate, then select and improve prospective investment properties:

1) Macro-Location: Markets with Declining Vacancies and Rent Growth – sometimes even CAP rate compression. As home ownership becomes less affordable, or foreclosures increase (as in many US markets) demand increases for rental housing. This in turns decreases vacancies, increases rents and increases values in select markets such as SK, CO, AZ, TX .. even some ON markets .. see chart on page 10 above ! Until recently, rent growth, declining vacancies and CAP rate compression was attainable in Alberta. However, with vacancies and CAP rates as low as they will likely go, CAP rate compression and high leverage with positive cash flow are no longer possible, only very slight rent growth is attainable. Hence, re-finance and hold most of your AB or SK properties and focus on new areas that meet these three criteria such as select pockets in Saskatchewan, B.C., ON, CO, AZ and Texas.

2) Micro-Location: Property Under-Valued with Upside (class “C” building in class “B” location). Buy in sub-markets that are desirable to live in. Would we personally live in that location? Would my daughter live here? Is this an area of positive transition ? Are there transportation improvements coming? Is there a Starbucks, a shopping centre, a desirable school or a park nearby ? Is this an area where “average” people want to live in?

3) Property Upgrades: In addition to buying in desirable sub-markets of growth markets, also improve the properties with appropriate spending. Look for assets that have higher than normal vacancies when you purchase, due to management neglect or poor spending by the previous owner. We then apply better management and marketing techniques (which cost relatively little) and also apply prudent spending as depicted earlier on page 6. The spending varies from inexpensive (like paint, clean-up, a new sign or cutting the grass) to full renovations in-suite or on common areas like hallways or exteriors – depending on the project.

4) Positive Cash-Flow with High Leverage (which is a function of going in CAP rate and debt coverage). Over the last few years in Alberta or Saskatchewan, investors have been able to create positive cash flow with a high leverage mortgage (i.e. typically 80 to 85% loan-to-value). With real estate prices so high in AB and now SK relative to rents, it is very difficult (even impossible) to find these types of properties. In select pockets of Canadian or US growth markets, you can still find these buildings!

Using these proven four approaches, you can repeatedly deliver high double digit to often triple digit returns on the cash invested .

Why Invest in Apartment Buildings (and not shopping centers or office towers)

1) High ratio and inexpensive financing (up to 80% loan-to-value is available).

2) Given strong in-migration, high house prices and rising interest rates there is substantial demand for affordable rental properties.

3) Like many urban areas of Central Canada, Coastal USA, or Europe, renting is the economic choice once ownership costs like utilities, condo fees, and/or mortgage payments are beyond the reach of the average blue collar worker, senior or college student.

4) Major infrastructure projects, new factories and expanding businesses/colleges are luring workers, students and seniors alike in SK, CO, AZ and TX with plenty of job opportunities, decent wages, low taxes and affordable rents.

5) The multi-family rental investment market trades well below replacement cost.

6) Without cash-flow, a real estate investment is more risky (such as development deals, international vacation properties, condo conversions, and land development deals). Go for boring, stable, predictable 15-20% annuallized returns for a long, long time. True wealth is created through long term asset ownership, not through speculative flips. Yes, in 2020 or 2030 we still have renters, and guess what: rents will likely be much higher than today!

The article above courtesy of Prestigious Properties President Thomas Beyer.