“At a time where Yves sees investment gurus shouting to steer clear of Treasuries and move into stocks, he feels that investors are being misled; he does not roll over to the common belief that stocks will outperform bonds from here as recent market and economic developments have prompted a change in investor attitudes.

ks?”

Quotable

“Arbitrary power is most easily established on the ruins of liberty abused to licentiousness.” – George Washington

FX Trading – Central Bankers Seek a Dollar Bottom; Bonds Favored Over Stocks?

The Bank of England last week made comments regarding some recent weakness in the British pound. It was seen as a potential boost to the UK economy as they’d love to resuscitate what external demand for their exports, albeit a relatively small portion of their economy.

There seems to be ongoing concern from the Swiss National Bank that the value of the franc is becoming too high, versus the buck and the euro. It has been stated that they will use the franc to help guide monetary policy.

In Japan, it seems to be a teeter-totter of comments that may or may not mean the Bank of Japan will take steps to stem the rise of the yen versus the US dollar.

And the latest among central bank intervention talk comes out of the EU, where Eurozone finance ministers are set for this weekend to discuss appreciation of the euro exchange rate.

The EU comments were icing on the cake and bring to light the concern among foreign policy-makers that their currencies have become too strong in light of the US dollar’s recent sharp decline.

Will that be enough to provide a bottom for the US dollar? Maybe in the short-term, at least. It could prompt traders and investors to cover their short positions, which could help to build some momentum to the upside.

Looking at the US dollar Index, 80 seems to be a good stopping point if this nascent correction has any legs. That level is an area of past support and resistance …

Looking at global economic fundamentals, nothing has really changed to favor the US dollar. Sure, we can draw on many of the same items that could eventually provide some fuel for a dollar rally if it gets a major risk-aversion bid. But the signs pointing to recovery continue to surface and lend credibility to optimists who are more than willing to take on risk.

But this change in sentiment among policy-makers could induce the US dollar correction that appears overdue. If this happens, then attention will turn to global market sentiment … looking for any obvious changes on the risk-appetite front.

_________________________________________________________________________

Yves Lamoureux – Blackmount Capital

Negative risk premium and return assumptions.

Yves Lamoureux of Blackmont Capital Inc. seems to think too much emphasis is being put on relatively minor shifts in risk appetite, specifically as it concerns the bond market.

At a time where Yves sees investment gurus shouting to steer clear of Treasuries and move into stocks, he feels that investors are being misled; he does not roll over to the common belief that stocks will outperform bonds from here as recent market and economic developments have prompted a change in investor attitudes.

ks?

The Bank of England last week made comments regarding some recent weakness in the British pound. It was seen as a potential boost to the UK economy as they’d love to resuscitate what external demand for their exports, albeit a relatively small portion of their economy.

There seems to be ongoing concern from the Swiss National Bank that the value of the franc is becoming too high, versus the buck and the euro. It has been stated that they will use the franc to help guide monetary policy.

In Japan, it seems to be a teeter-totter of comments that may or may not mean the Bank of Japan will take steps to stem the rise of the yen versus the US dollar.

And the latest among central bank intervention talk comes out of the EU, where Eurozone finance ministers are set for this weekend to discuss appreciation of the euro exchange rate.

The EU comments were icing on the cake and bring to light the concern among foreign policy-makers that their currencies have become too strong in light of the US dollar’s recent sharp decline.

Will that be enough to provide a bottom for the US dollar? Maybe in the short-term, at least. It could prompt traders and investors to cover their short positions, which could help to build some momentum to the upside.

Looking at the US dollar Index, 80 seems to be a good stopping point if this nascent correction has any legs. That level is an area of past support and resistance …

US Dollar Index, Weekly

Looking at global economic fundamentals, nothing has really changed to favor the US dollar. Sure, we can draw on many of the same items that could eventually provide some fuel for a dollar rally if it gets a major risk-aversion bid. But the signs pointing to recovery continue to surface and lend credibility to optimists who are more than willing to take on risk.

But this change in sentiment among policy-makers could induce the US dollar correction that appears overdue. If this happens, then attention will turn to global market sentiment … looking for any obvious changes on the risk-appetite front.

Yves Lamoureux of Blackmont Capital Inc. seems to think too much emphasis is being put on relatively minor shifts in risk appetite, specifically as it concerns the bond market.

At a time where Yves sees investment gurus shouting to steer clear of Treasuries and move into stocks, he feels that investors are being misled; he does not roll over to the common belief that stocks will outperform bonds from here as recent market and economic developments have prompted a change in investor attitudes.

Most market participants today still expect a positive risk premium for stocks even if extrapolating from recent past events results in confounding this expectation.

I expect bonds to deliver better or equal real returns with fewer risks than stocks going forward. Negative risk premium is the new normal and new behavioral shifts strongly underpin that case.

I had originally offered my case to buy the long bonds near the bottom of this cycle on the 19th June. http://yelnick.typepad.com/yelnick/2009/06/yves-on-the-greenshootfed-sacred-fed-bull-died-fat-and-happy.html

You create a spread of 4% or better between the Fed fund and the long bonds and in turn that becomes a trading buy signal. We had such a signal and ran with it.

We continued to run with this message digging further and came up with the primary dealers’ net treasury weekly positions graph in relations to bonds. What we found was most unusual. After averaging a net short position of -60 billions on average over many years, the primary dealers had suddenly turned bullish with net long treasury positions.

http://www.zerohedge.com/article/guest-post-observations-unusual-bond-deal-behavior

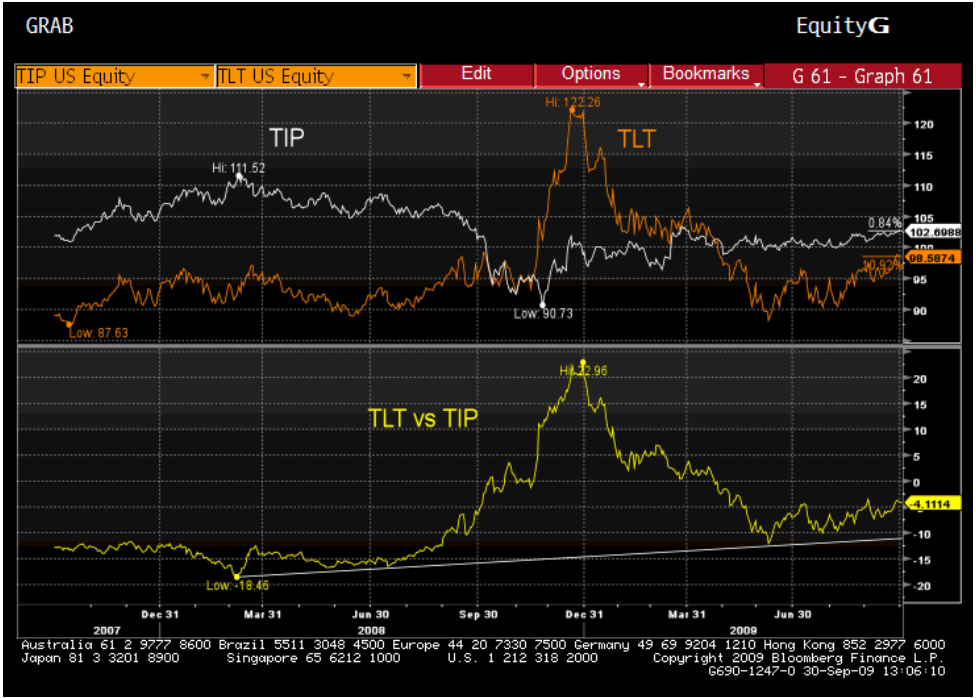

In this next graph, I use TLT as a proxy for long term bonds and TIP as the proxy to represent the Treasury inflation protected bonds. The recent recovery points to TLT showing greater strength and the clear conclusion is one of deflation reasserting itself or the lack of inflation thereof.

In a negative risk premium world you would expect to have bonds outperform stocks for total return and the yellow line here (below) where bonds are compared to the S&P500 is definitely up.

From both charts long bonds are definitely turning up or have put in a good base from which to launch upward.

In reference to behavior, it’s become clear that investors attitude are changing and the new normal is not to invest one’s savings in stocks rather that money is flowing to bonds. Recent data points to exactly this type of behavior and perhaps getting trounced once is enough for a certain legion of investors but not all. As we had seen in 2000 in every drop of stocks, we are slowly loosing participants to join in this exuberant party. Investors who miss out this time are also assured of not feeling any party hangover.

Yves Lamoureux,

Investment Advisor,

Blackmont Capital Inc.

John Ross Crooks III

Black Swan Capital LLC

www.blackswantrading.com

Black Swan Capital is an independent minded currency advisory firm established to provide subscription-based services to help retail and institutional clients consistently attain above average profits trading and investing in both forex and currency futures markets. We tell our Members when to enter and exit and why. HERE for more information.

Our commitment is to deliver well researched trading recommendations that our clients understand and can efficiently execute through their brokers. We outline the reasons to enter a trade and define the risk. But our Members must understand there is a substantial risk of loss trading in forex (off-exchange retail foreign currency) and currency futures markets.

Register HERE for the FREE Daily Currency Currents Newsletter.As a subscriber to Currency Currents you stay tuned-in to our current global-macro view and our analysis of key investment themes driving currency prices. Nothing is off limits to us in this free-wheeling look at the markets. Some days you’ll receive ramblings on trading psychology, while other days we may take an academic approach in explaining esoteric economic issues. Ultimately we have one goal in mind: to help you get a handle on the key investment themes driving global capital flow. Because if you know where the money is going, it increases the probability that yourposition in the market will be a profitable one.