From BHP Billiton’s mid-year presentation, here are the three reasons they’re concerned about what the future holds.

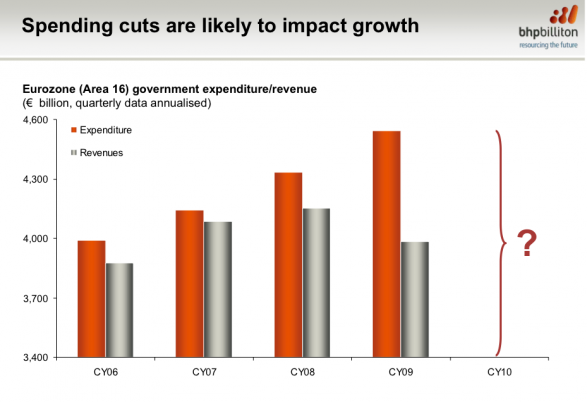

First, austerity

Second, debt levels.

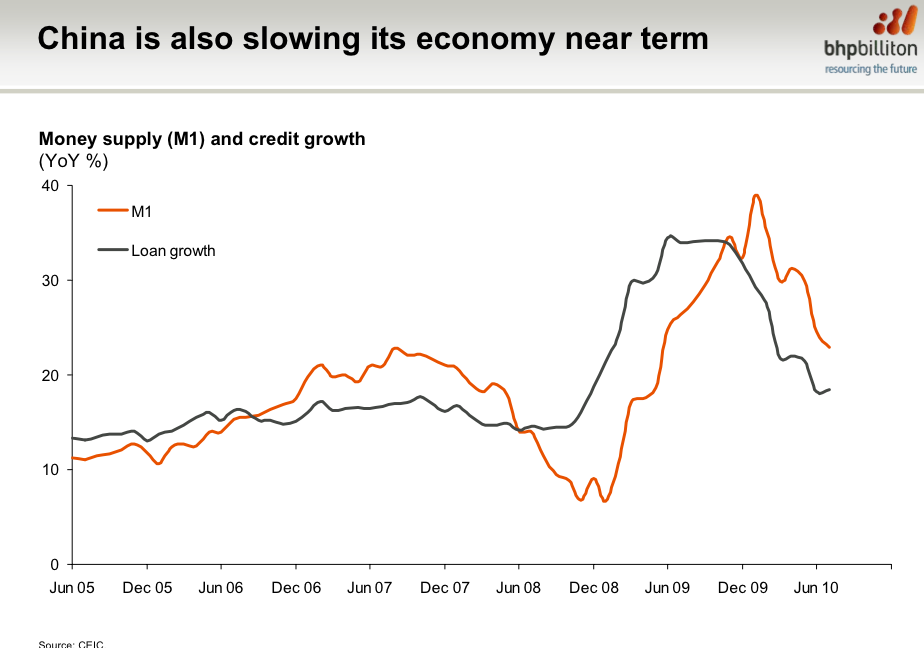

And third, China.

BHP Sounds The Alarm On Global Growth And Commodity Prices

How does the world’s biggest miner, and the possible acquire of Potash for $39 billion, see the global outlook?

They’re pretty nervous. The following comments come from the company’s mid-year report.

….read it all HERE

YOU CALL THIS CAPITULATION?

by David Rosenberg

Short interest on the Nasdaq down 1.6% in the first week of August? The Rasmussen investor confidence index at 80.4? Call us when it hits 50, which in the past was a “classic” washout level.

Investors Intelligence did show the bull share declining further this past week, to 33.3% from 36.7%. But the bear share barely budged and is still lower than the bull share at 31.2%. Are we supposed to believe that at the market lows, there will still be more bulls than bears out there? Hardly. At true lows, the bulls are hiding under table screaming “uncle!”.

Yes, Market Vane equity sentiment is down to 46, but in truth, this metric is usually in a 20-30% range when the market correction ends. We are waiting patiently.

As for bonds, well, Market Vane sentiment is 73%. Now what is so bubbly about that. Call us on extreme positive sentiment when this measure of excessive bullishness is closer to 90%, and we’ll be in the correction camp hopefully by the time this happens.

In any event, the extent of the denial over U.S. double-dip risks is unbelievable. These are quotes from economists and strategists in yesterday’s print media — and just a select list at that for there was just so much surreal commentary: “I’d be shocked if you don’t make a lot money in U.S. stocks over the next decade.”

“If yields rise, then 30-year bonds will suffer.”

“It won’t be a double-dip recession but it might feel like it.” “There is a global perception that we are not necessarily going into a Japan-type scenario, there is a recognition of a slow recovery.” “People shouldn’t panic.”

At market lows, the recession rhetoric becomes more intense and indeed it’s when people do panic that the best buying opportunities generally occur.